Select date

Media Focus on Trump Blindsides the Public from Rising Wall Street Risks

by Pam Martens and Russ Martens, Wall Street On Parade:

There are some very serious undercurrents at work in the U.S. financial markets but they are getting short shrift on the front pages of newspapers as the President’s travails dominate the news. That’s working out well for Wall Street, which wants to keep the public slumbering as long as possible in hopes of gutting more financial regulations.

One of those serious undercurrents is the amount of risk being held by the biggest banks in the country. According to the Federal Reserve’s release of its Supervisory Stress Test, of the 34 Bank Holding Companies that are subject to its review, under a “severely adverse scenario,” meaning a deep recession, losses for the combined group are projected to be $493 billion.

Not to put too fine a point on it but that’s just 34 banks out of a total of 5,856 FDIC insured banks in the U.S. according to the FDIC’s March 31, 2017 database. The federal deposit insurance fund as of March 31, 2017 has on hand only $84.9 billion to bail out all banks that go under. That means that if there is, once again, contagion among Wall Street mega banks because they’ve all crowded into toxic debt with derivatives written on top, the taxpayer will once again be dragged kicking and screaming by Wall Street cronies in Congress to bail out the reckless bad boys on Wall Street and their multi-million dollar bonuses — which are somehow sacrosanct even when the recipients have put the nation in financial crisis.

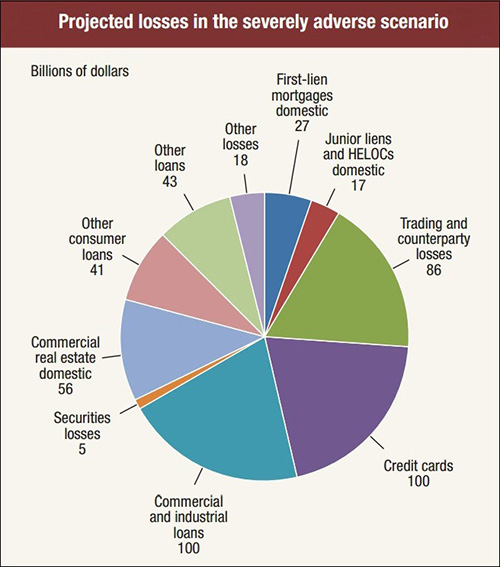

The chart above from the Fed’s Supervisory Stress Test shows just how dangerous and irrational the U.S. financial system has become. The traditional role of banks to lend money to commerce and the consumer to keep the economy expanding and innovating and creating good jobs for Americans has been co-opted by Wall Street’s desire to trade and speculate and, eventually, blow itself up again.

The numbers in the chart above represent billions of dollars of projected losses. The losses from trading events and counterparty losses on derivatives are projected at $86 billion versus $100 billion in projected losses on commercial and industrial loans – the core function of a bank.

Unfortunately, the public cannot trust the projected trading and counterparty losses from the Fed. We know that from the experience of 2008 when the Fed turned out to be the dumb tourist when it came to anticipating the hundreds of billions of dollars in derivative losses hiding in the dark corners of Citigroup and AIG and Lehman Brothers — and Goldman Sachs had AIG not been bailed out. We also know from our previous reporting that the Fed is currently standing down when it comes to reining in derivative risks escalating at the biggest Wall Street banks. (See our related articles below.)

There’s also something specious about how the Fed calculated this $86 billion anticipated trading and counterparty loss. It says “these projected losses are based on the trading positions and counterparty exposures held by these firms on a single date (January 3, 2017) and could have differed if they had been based on a different date.” Why wouldn’t the Fed project losses for a dozen or so different dates and then take the average? January 1 is a holiday and January 3 is just two days into the new trading year when banks are unlikely to have had time to have taken on significant risks.

We reported in March of last year on the concentrated risk for derivative contagion. We wrote: