Select date

The Coming Carmageddon

by David Stockman, DailyReckoning:

Ben Bernanke’s successors at the Fed and other global central banks still don’t get it.

Ben Bernanke’s successors at the Fed and other global central banks still don’t get it.

Falsified debt prices do not promote macroeconomic stability. They lead to reckless credit expansion cycles that eventually collapse due to borrower defaults. We’re now seeing that play out in the auto sector, especially since anyone who can fog a rearview mirror has been eligible for a car loan or lease.

If that reminds you of the sub-prime housing disaster, you’d be right.

That, in turn, will make the looming collapse even worse, due to the sudden drastic shrinkage of credit in response to escalating lender losses.

How did we get here?

Let’s start by looking at the Fed. Its reckless monetary reflation cycle in response to the Great Recession caused auto credit, sales and production to spring back violently after early 2010.

Accordingly, that reflation has powerfully impacted the growth rate of total U.S. domestic output. And it’s had a massively distorting effect.

Auto production has seen a 15% gain over its prior peak, and a 130% gain from the early 2010 bottom. But overall industrial production is actually no higher today than it was in the fall of 2007. Real production in most sectors of the U.S. economy has actually shrunk considerably.

That means if you subtract the auto sector, there has been zero growth in the aggregate industrial economy for a full decade.

So the auto industry has actually distorted the effects of monetary central planning.

But the real point here is that the financial asset boom-and-bust cycle caused by monetary central planning is making the main street business cycle more unstable, not less. And it means the next auto cycle bust is certain to be a doozy.

It also means the weak expansion of real sales and GDP over the past seven years has been artificially supported by a rapid but unsustainable snapback in the auto sector. But that is now over.

And what I call Carmegeddon will soon be now metastasizing rapidly.

Consider that credit analysis in the auto sector is now being overwhelming driven by the collateral value of the vehicle — not the creditworthiness of the borrower.

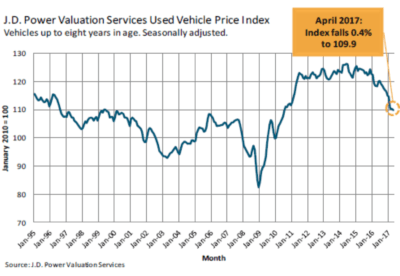

Accordingly, when car prices fall sharply, losses from loan defaults will soar. During the last cycle, used car prices peaked in early 2006 and then fell nearly 25% through the 2009 bottom. Total auto credit cratered during the same period.

And today, after plateauing for more than two years, used car prices have now begun a steep descent. During April, for example, prices of most classes of used vehicles plunged sharply. The J.D. Power index was down 13%. Needless to say, the drop in used car prices is now accelerating.

But it still has a long way to go due to the rising tide of used cars from maturing leases and loans that are hitting the markets.

Looking back to the last credit cycle, the crash of new cars sales after 2007 resulted in a drastic shrinkage of leased vehicles. Accordingly, volumes of pre-owned vehicles hitting the used car auctions hit a modern low of 13 million vehicles during 2011-2013. That supply shortage obviously fueled a sharp rebound of used car prices.

By contrast, the post-2010 auto sales boom is now generating an all-time record tsunami of pre-owned vehicles. During the period 2016-2018, an estimated total of 21 million used vehicles will have hit the market.

That 62% surge in used vehicle supply has clear, negative implications for used car prices.

The most immediate negative effect of plunging used vehicle prices, of course, is sharply reduced values among leased vehicle portfolios. That, in turn, not only results in losses for equity holders, but also causes monthly payment rates to rise sharply on new leases.

Lease volumes dropped by 45% during the last down cycle. But at current all-time highs of 4.3 million newly leased vehicles last year, volumes could drop by upwards of 70% during the years just ahead.

Indeed, more than 30% of new vehicle sales were leased in 2016. And the all-time record of 4.3 million new leased vehicles in 2016 was nearly double the 2007 peak, and 4X the 2009 bottom.