Select date

Risk has been Abolished, According to Institutional Investors

by Wolf Richter, Wolf Street:

![]() Why? Wall Street sells “more financial products and generates more profits when investors are bullish.”

Why? Wall Street sells “more financial products and generates more profits when investors are bullish.”

“Covenant-lite” loans – risky instruments issued by junk-rated borrowers, with few protections for creditors – set an all-time record at the end of the second quarter.

They’re part of the risky universe of “leveraged loans,” and they’re secured by some collateral, but they don’t come with the protections and restrictive maintenance requirements in their covenants that traditional leveraged loans offer creditors.

Even leveraged loans with more restrictive covenants are so risky that banks just arrange them and then try to off-load them to institutional investors, such as pension funds or loan funds. Or they slice and dice them and package them into Collateralized Loan Obligations (CLOs) and sell them to institutional investors. Leveraged loans trade like securities. But the SEC, which regulates securities, considers them loans and doesn’t regulate them. No one regulates them.

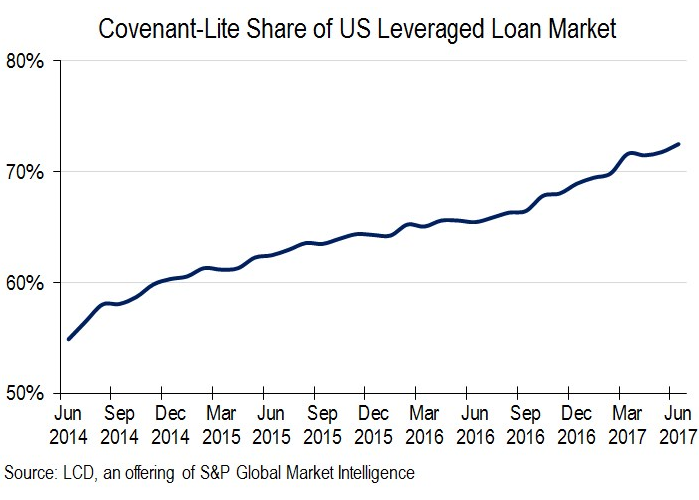

The amounts are not trivial. Total outstanding leveraged loans in the US reached nearly $1 trillion ($943 billion) at the end of the second quarter, according to S&P Capital IQ LCD. And covenant lite loans made up 72.5% of them, the highest proportion ever.

That’s up from 69% at the end of the fourth quarter. This chart shows the surge in the proportion of covenant-lite loans to total leveraged loans over the past three years, from about 55% at the end of Q2 in 2014 to 72.5% at the end of Q2 2017:

So what’s the big deal? When there is no default, there is no difference. And since there is apparently no longer any risk of default, it’s, well, no big deal. That’s what investors are thinking.

But when defaults do occur – as they have a nasty tendency to do – or before they even occur, investors have less recourse and fewer protections, and losses can be much higher.

The Fed and the OCC have been jawboning banks into backing off with leveraged loans for three years. Banks can get stuck with leveraged loans. They did during the Financial Crisis, which helped sink the banks. That’s when investors found out that leveraged loans are not exactly, as they say, as good as gold. But back then, the proportion of covenant lite loans was much smaller. So next time, the ride will be wilder.

Why do investors do this? They’re chasing yield, little else matters, and companies take advantage of that. LCD about the covenant lite loans:

For obvious reasons, they are more attractive to issuers, and have gained steady acceptance from loan arrangers [banks] and investors, particularly since 2012, when the US leveraged loan market found a higher gear after the financial crisis of 2007-08.

Then again, as naysayers are fond of pointing out, they’ve never comprised this much of the market before, so they will be under scrutiny once the current credit cycle turns.