Select date

Paul Krugman, the Federal Reserves and the Fatal Conceit of Keynesian Economics

by Peter Schiff, Schiff Gold:

A recent Paul Krugman New York Times column praised the success of the Keynesian macro model in the wake of the 2008 financial crisis. In his view, the Federal Reserve did exactly what was necessary – pushed interest rates to zero and launched rounds of quantitative easing to jumpstart demand. As Tom Woods and Bob Murphy put it in a recent episode of the Contra Krugman podcast, “we agree that Krugman’s model did great…if we overlook all the times it blew up in his face.”

A recent Paul Krugman New York Times column praised the success of the Keynesian macro model in the wake of the 2008 financial crisis. In his view, the Federal Reserve did exactly what was necessary – pushed interest rates to zero and launched rounds of quantitative easing to jumpstart demand. As Tom Woods and Bob Murphy put it in a recent episode of the Contra Krugman podcast, “we agree that Krugman’s model did great…if we overlook all the times it blew up in his face.”

As is typical of Keynesians, Krugman ignores the side-effects of Federal Reserve policy. It works for a while, but it perpetuates the boom-bust business cycle. Sure, the economy today seems to be booming, but there is a rotten underbelly that most everybody in the mainstream seems to be ignoring. Peter Schmidt offers a succinct breakdown of Keynesian-based Fed policy and reveals why its doomed to failure.

The following was written by Peter Schmidt. Any views expressed are his own and do not necessarily reflect the views of Peter Schiff or SchiffGold.

![]()

Paul Krugman has a BA from Yale and a PhD from MIT – both in economics. From his perch at the New York Times, he has an almost unrivaled ability to dispense economic advice. Because he constantly views economic events through a political prism, his advice on contemporary economic issues is completely devoid of merit. Paul Krugman may be a lot of things, but an original thinker he is not. In December 2000, he spoke for the economic establishment in academia, on Wall Street and at the Federal Reserve when he said,

The point is that recessionary tendencies can usually be effectively treated with cheap, over-the-counter medication: cut interest rates a couple of percentage points, provide plenty of liquidity, and call me in the morning.”[i]

In Paul Krugman’s view of the world, the Fed has the amazing ability – merely by manipulating interest rates – to inerrantly guide the economy. It only takes a cursory review of economic history to show how laughable this idea is. The two biggest economic disasters to befall the United States – the Great Depression and the Great Recession of 2008 – both occurred after the Federal Reserve was formed. If the economy could be controlled with the contemptuous ease with which a doctor treats the common cold, then how could these two economic calamities occur with the Fed manipulating interest rates in exactly the way Krugman describes?

Indeed, Paul Krugman’s endorsement of an “active” central bank controlling the economy with the same level of precision a pilot uses to land a 747 is completely contradicted by Paul Krugman! Writing in October 2002, Paul Krugman praised the Federal Reserve of Alan Greenspan and Ben Bernanke for cutting rates and increasing liquidity after the tech bubble burst. Here is Krugman in his own words,

It’s true that Alan Greenspan and his colleagues made a much better start than their counterparts in Japan. They knew that the Bank of Japan cut interest rates too slowly, and that by the time it realized the seriousness of the country’s problems it was too late: even a zero interest rate wasn’t enough to spark a recovery. So the Fed cut rates early and often; those 11 interest rates cuts fueled a boom both in housing purchases and mortgage financing, both of which helped keep the economy from experiencing a much more severe recession.” [ii]

The interest rate cuts that Krugman celebrates here were not fueling a ‘boom in both housing purchases and mortgage financing;’ they were fueling the terminal stages of the largest financial bubble in US history – the housing bubble. In terms of homeownership, the US housing bubble peaked not long after Krugman put these error-riddled thoughts to paper; April 2004. To be sure, the Federal Reserve wasn’t the only organization responsible for blowing up to the housing bubble. Enormously important roles were played by Bill Clinton, his two housing secretaries – Henry Cisneros and Andrew Cuomo, Wall Street, the two completely inept political cronies placed in charge of Fannie Mae [iii], and many members of Congress to name some of the most prominent.

However, it was the Federal Reserve alone that conjured out of thin air the credit money which provided the rocket fuel to send home prices and homeownership rates into the stratosphere. Without the Fed actively manipulating interest rates, there was a limit to how big the housing bubble could grow. With the Federal Reserve slashing interest rate as a matter of policy, there was virtually no limit to how big the housing bubble could grow. As it turned out, the only limit on the size of the housing bubble would be the number of otherwise insolvent borrowers who obtained mortgages. Once all the insolvent borrowers had their loans, there was nothing to force home prices higher. Once home prices simply stopped increasing [iv], the economy was doomed.

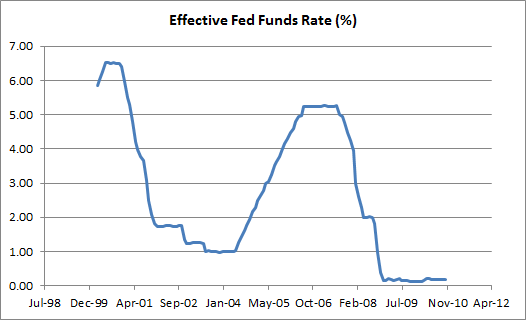

In the chart above, interest rates set by the Fed are plotted. This chart captures the Fed slashing interest rates after the March 2000 collapse of the tech bubble, and then embarking on another interest rate slashing exercise in July 2007 when sub-prime mortgages first started to take on water. Do these interest rates appear to be the product of some well-thought-out policy? Do these interest rates appear to mimic the way a doctor might dispense medicine? More than Paul Krugman’s praising the interest rates cuts as fuel for the housing bubble, this chart completely exposes the notion that the Fed can guide the economy by actively manipulating interest rates as completely fraudulent.

It should be obvious that the foundation of modern economics is built on the soft sands of an erroneous fatal conceit; the ability of an all-powerful, all-knowing central bank to control the economy by manipulating interest rates. One of the many ways in which the study of economics differs from useful fields like physics or mechanical engineering is the failure of economists to learn from their mistakes. (Because so many economists, like Paul Krugman, graduate from schools like Yale and MIT they don’t even admit mistakes – which makes learning from them impossible.)

Loading...