Select date

It Ain’t So, Alan! Why Greenspanian Central Banking Is the Mortal Enemy of Capitalist Prosperity

by David Stockman, via Lew Rockwell:

We can thank bubblevision and the Maestro himself for a splendid reminder today that Greenspanian central banking is the greatest menace to capitalist prosperity ever invented. This was made abundantly clear by his pronouncement on CNBC regarding the current labor market:

“Tightest labor market I’ve ever seen.” – Greenspan on

@CNBC

As an empirical matter, of course, that’s rank nonsense – and is among the stupidest quips the Maestro has ever uttered. That’s because the law of supply and demand dictates that if the labor market is actually the tightest since Greenspan began his career in the 1950s, wage rates should also be rising at the highest rate ever.

In fact, at 2.8% year-year-over year for September 2018, nominal wage growth (red line) is the lowest it’s been since the late 1960s; and in real terms, the story is even worse.

To wit, between 1955 and 2000, real compensation per hour grew at a 1.75% annual rate – and that’s the average across seven business cycle, including recession years.

By contrast, we are now at the top of the second longest business expansion in history, and real compensation (purple line) was up just 0.7% over the past 12 months. And that’s virtually the weakest late cycle growth rate on record.

In short, the only valid free market measure of “tight” is the price of labor, and those limpid wage rates say absolutely not.

Of course, what the Maestro and his Keynesian fellow travelers refer to is not the verdict of the marketplace, but bureaucratic guesstimates about labor market conditions published monthly by the BLS. Yet it doesn’t take even 10 minutes worth of investigation to show that the BLS’ tightness gauge – the U-3 unemployment rate – is not worth the paper it’s printed on.

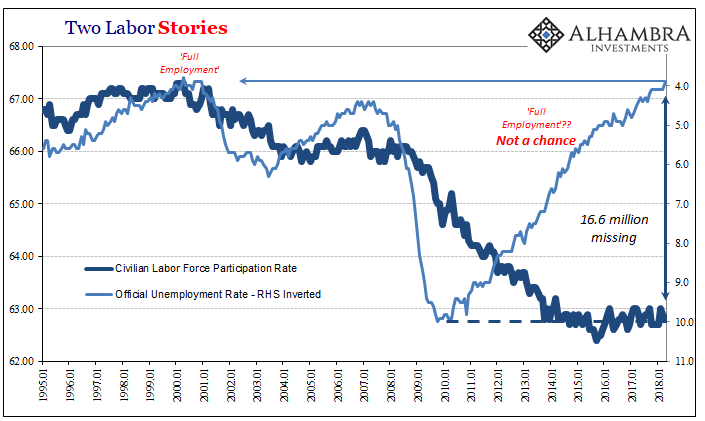

As Jeff Snider has cogently demonstrated, we are at 3.7%unemployment only because the labor force participation rate as measured by the BLS has plunged.

In fact, at the same 3.7% so-called full employment rate which pertained when the Maestro was riding high in the late 1990s, the labor force participation rate was north of 67%, not today’s 62.7%(September). And that means the Maestro’s alleged labor shortage rests on the back of 16.6 million workers who have purportedly gone missing!

We don’t think any workers have actually gone missing at all, and believe that the actual unemployment rate is upwards of 40%, as demonstrated below. But suffice it to say here that there is a reason why Wall Street and Washington economists alike insist on using the patently ridiculous and grossly erroneous numbers manufactured by the BLS data mills.

To wit, the BLS jobs data – and especially the U-3 unemployment rate – function as a convenient “help wanted” sign for Keynesian interventionists. The implication is that the free market’s pricing system for labor, goods and services doesn’t work very well, and that the wise guiding hand of the state is needed to regulate an economic ether called “aggregate demand”.

That is to say, the US economy resembles a giant economic bathtub, and the aim of government policy is to keep it filled exactly to the brim. That way, everybody’s got a job, a good wage, a nice life, no (inflation) worries and perhaps is even rid of sniffles and hangnails, too!

So when the U-3 unemployment rate is at 11%, 8% or 5%, there is purportedly a large deficiency of demand, signaling that the state and its central banking branch need to pump more spending into the bathtub via fiscal or monetary stimulus.

Likewise, when U-3 reaches the alleged “full employment” rate at + /- 3.7% that’s a signal the tub is close to full and that interest rates need to be raised in order to curtail credit expansion and spending, thereby insuring that an inflationary overflow does not upset the macroeconomic applecart.

But here’s the thing. The 12 members of the FOMC might as well be standing out on Independence Avenue waving their arms in order to keep marauding elephants from overrunning the Eccles Building!

That’s about how useful U-3 is as a measure of labor market or macroeconomic conditions; and it’s also about as worthless as is the Fed’s endless pegging of money market rates and massive intrusion in the bond markets in furtherance of capitalist prosperity.

The fact is, the potential labor supply from both domestic and offshore sources is so limitless that the only thing needed to mobilize more employed hours is the pricing system, not the monetary politburo’s (FOMC) machinations in the financial markets.

At a high enough wage rate, you will get housewives out of the kitchen, students off their duffs, more volunteers for overtime, and, if need be, more peasants out of the Chinese or Vietnamese rice paddies. In today’s globally networked, traded and welfare-enabled world, there will never be a physical shortage of labor hours – just the right price to bring latent hours into monetized production.

Needless to say, the latent hours now sequestered in Federally subsidized basket-weaving classes or playing shuffleboard on early retirement or disability do raise market-clearing wage level s at the margin. But you can solve that problem but cutting welfare benefits, not giving the Fed a mandate to fiddle with interest rates and financial asset prices.

That latter only fosters increasingly destructive gambling, bubbles and malinvestments in the financial system, not higher production, employment and prosperity on main street.

Loading...