Select date

Ultra-Low Mortgage Rates No Relief for Home Sales

by Wolf Richter, Wolf Street:

![]() Surging prices are a demand killer, but real estate industry laments the medicine didn’t work.

Surging prices are a demand killer, but real estate industry laments the medicine didn’t work.

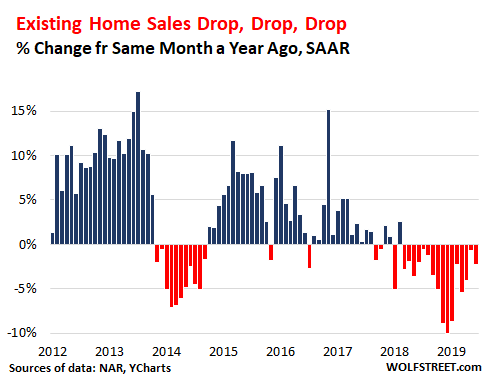

The relentlessness of falling home sales is starting to baffle the real estate industry that had expected plunging mortgage rates to fire up sales: Across the US, sales of “existing homes” (previously owned single-family houses, townhouses, condos, and co-ops) in June dropped 2.2% from June last year, to a seasonally adjusted annual rate of 5.27 million homes, according to the National Association of Realtors. It was the 16th month in a row of year-over-year declines (data via YCharts):

“Home sales are running at a pace similar to 2015 levels – even with exceptionally low mortgage rates, a record number of jobs and a record high net worth in the country,” lamented NAR’s report.

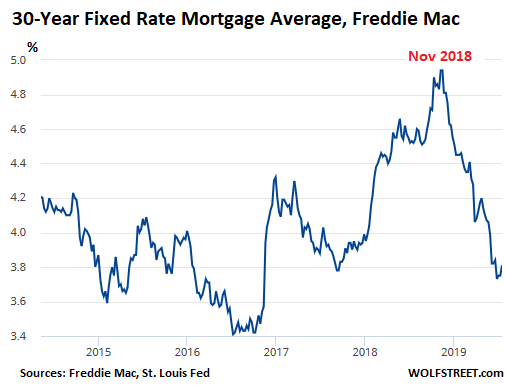

And the plunge in mortgage rates from the November high has been spectacular. The Fed has hiked rates one more time in December and so far has not cut rates. But yields across the curve have been dropping in anticipation of a veritable Niagara Falls of rate cuts and whatnot.

In June, the Freddie Mac average commitment rate for a 30-year, conventional, fixed-rate mortgage fell to 3.80%. This is over a full percentage point lower than the average rate in November of 4.87%:

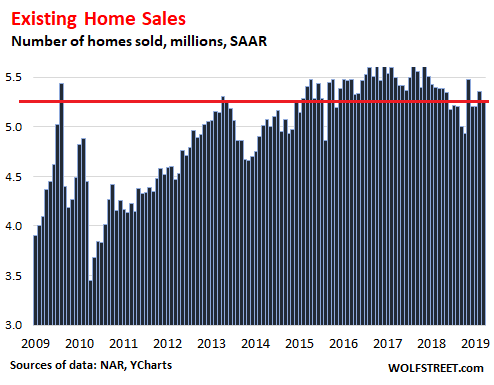

Sales of existing homes in June, at 5.27 million seasonally adjusted annual rate, are now back in the range where they’d been in 2015. The chart below shows how home sales topped out late 2017 and early 2018 at a pace above 5.5 million, as mortgage rates were already rising. When mortgage rates began ascending at a steeper slope, sales fell sharply, as you would expect, hitting the low point in December and January for deals signed in November and December.

But given the plunge in mortgage rates since then, expectations were that sales would resurge. While sales have ticked up from those lows, the move was, for the industry, confusingly feeble (data via YCharts):

The astonishment of the industry with these falling home sales despite ultra-low mortgage rates emerges in the report’s comment, as the industry is grappling with potential answers:

Either a strong pent-up demand will show in the upcoming months, or there is a lack of confidence that is keeping buyers from this major expenditure. It’s too soon to know how much of a pullback is related to the reduction in the homeowner tax incentive.

By home category: Sales of single-family houses in June fell 1.7% year-over-year to a rate of 4.76 million, and sales of condos and co-ops fell 6.5% year-over-year to a rate of 580,000.

Sales by region in June show the steepest year-over-year declines in the West and the Northeast:

- Northeast: -4.2%, to an annual rate of 680,000

- Midwest: -1.6%, to an annual rate of 1.25 million

- South: -0.4%, to an annual rate of 2.25 million

- West: -5.2%, to an annual rate of 1.09 million.

Inventory for sale in June was about flat compared to June last year. Given slower sales, supply at the current rate of sales ticked up to 4.3 months (from 4.0 months a year ago). This is plenty of supply. But it’s the wrong supply.

After years of price increases, home prices together have moved up the ladder, including the lower end that is now priced where mid-range used to be a few years ago, and there is no more “low end” in many markets, and the new low end has moved out of range for many buyers. High prices kill demand. And low mortgage rates, after years of low mortgage rates, are having only a limited effect on sales volume.

But the median price of existing homes sold in June across the US – median means half sold for more and half sold for less – rose 4.3% from a year ago to a record $285,700.

Loading...