Select date

It’s The Pace Of Change That Kills You

by Chris Martenson, Peak Prosperity:

And it has now sped up beyond our means to control it

And it has now sped up beyond our means to control it

A treasured member of my family is in the process of dying right now. She has lived a full, rich life; but her passing is a sad affair for us.

I’ve spent a lot of time recently with hospice workers. I’ve learned that they’re often asked by their patients, “How much time do I have left?”

While sometimes loathe to offer an answer, hospice staff can predict the timing of the end pretty accurately.

They do so by measuring by the changes they see. Or, more accurately, the pace of change in those changes.

Could a patient pick a book up off the floor in June, but not in July? If not, then their remaining time is likely to be measured in months.

Could they raise themselves out of a chair last week but not today? If not, then it may be only weeks until the end.

Are they losing function every day? Then death is likely just days away.

And so on, right through hours, minutes and seconds.

It is the pace of change that matters. Tracking the pace of change is as important as the actual changes themselves.

Both provide critical information about what’s going on, but it’s the pace that informs our timing predictions.

This is equally true for larger systems like economies and ecosystems.

The Pace Is Accelerating All Around Us

Losing a certain population of a given species over a million years is a very different proposition from losing the same number within just 40 years. Or even yearly, as now appears to be the case.

The years 2016, 2017, 2018 and 2019 each saw one or more Cat 5 hurricanes form in the Atlantic. This is the longest such stretch of years in the record books.

Dorian was absolutely brutal to the Bahamas; the damage was unprecedented and extreme. I simply cannot imagine the sustained horror of being pinned down by a Cat 5 for 36 hours as it brutally dismantled my home.

Like slow-moving Hurricane Harvey (not a Cat 5, but hugely damaging) Dorian just parked itself over the Bahamas and laid waste to all that lay beneath, churning like a massive blender.

Are monster storms that move slowly a new meteorological trend? Or has it simply been ‘bad luck’ to experience so many of late?

We don’t know yet. But there have only been 35 Cat 5 hurricanes in the past 100 years. However, at our current pace, there will be 125 such storms over the next century. That’s four times as many vs the past.

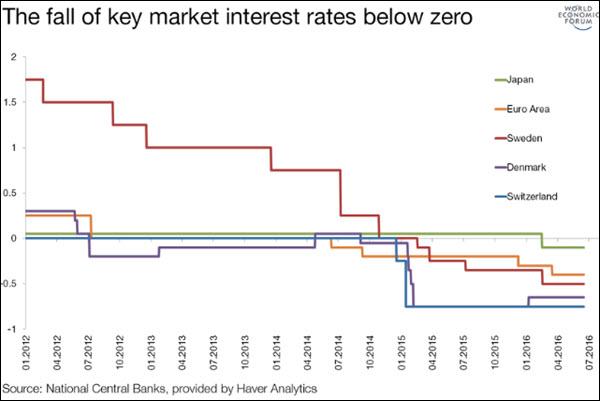

Negative Rates Multiplying At A Staggering Rate

Financially, the latest and most head-spinning change concerns the explosive proliferation of debts with negative interest rates.

Unheard of since the Mesopotamian invention of debt in 2,400 BC, negative interest rates have suddenly appeared on the financial landscape like a new mutant species, an invader without natural predators, gaining a sudden foothold and then spreading rapidly.

It’s as if a virulent chestnut blight landed in a virgin forest of corporate and sovereign debt.

From literally ‘none’ ten years ago, to more than $17 trillion now. And up from a ‘mere’ $6 trillion in the past ten months alone:

Is this a new, permanent trend? We don’t know yet.

But the pace of change is sure intensifying.

First, Switzerland gave negative rates a tentative go. Then Denmark timidly followed. But eventually, the entire Euro complex followed with gusto, with most countries’ rates crossing below the 0%-boundary in late 2014:

Whatever the final repercussions are, one fact is clear: the world’s central banks are completely, 100% responsible for these bizarro-world negative interest rates.

They try to pretend that the $20+ trillion money printing spree they engineered after 2008 isn’t a root cause. Instead, they claim “the markets” are responsible. But this is as weak a defense as Ted Bundy claiming his victims all killed themselves. It’s just not a credible defense.

Emboldened by seeing that nothing terribly bad happened in the early years of negative rates, the ECB went on an absolute tear of a printing spree in 2016 and 2017. It went so far as to buy corporate debt via private placement, meaning that the debt was never issued to the bond market. The ECB just conjured up the necessary billions of euros and directly credited corporate accounts while taking their bonds onto its books.

Again, it’s worth noting just how unusual this all is. It has never been done before.

5,000 years of accumulated knowledge is being chucked out the window by activist central bankers who assume they know best.

But do they? And what will be the repercussions if they don’t?

Economic And Social Vandalism

The financial media is working very, very hard to defuse concerns about negative rates and sell them as a talisman against anything that could hurt the economy.

They dutifully scribe down what the central bankers say, and then pitch it to us as gospel.

Instead, I propose that now is the time to ask stiff questions of the central bankers, and to not let them avoid answering. And to keep asking until we either receive reasonable responses, or clarify that they have no good answers to give.

Here are questions I would love to hear posed to Chairmen Powell, Draghi or Kuroda:

- “Your actions were designed to spike the prices of stocks and bonds and you’ve succeeded. This has led to an enormous wealth gap. What’s ‘too far’ in your view? Right now 5 people have as much wealth as the bottom half, by which we mean 3.8 billion humans. Is ‘too far’ when those same five individuals own as much as the bottom 75%? The bottom 90%? Or is it your aim that these top five individuals should actually possess everything in the world with everyone in their debt?”

- “5,000 years of financial trial and error has firmly established that saved capital deserves a positive rate of return. You are now certain that negative interest rates are what the world needs. What empirical data do you rely on to make that assessment? What happens if you’re wrong?”

- “All investment decisions depend upon an assumed rate of return. Pensions, for example, require matching future liabilities with current assets and an assumed rate of return. Now that central banks are certain that negative yielding debt is just what the doctor ordered, and under the principle of “you break, it you buy it“, we’re wondering what responsibilities the central banks are prepared to assume here for broken pensions?”

- “Same question as above, but for savers and endowments.”

- “Money is not actual wealth, but a claim on real wealth. More importantly, it’s a social contract. Central bankers are monkeying with that social contract and the effects are obvious. Corporations are incentivized to make returns by financially engineering their balance sheets and rigging their share counts instead of taking actual risks, hiring more people, and investing in R&D. Can we not just take this all the way to the end and propose eliminating risk for everyone and just give everybody money without anyone performing any work at all? Obviously not, but we’re also obviously somewhere along that path. The question is, how far is ‘too far’ and what criteria are you using to determine that?”

- “Endless growth is not possible on a finite planet. Your policies are all geared towards stoking the fastest economic growth possible. Do central banks have any responsibility to future generations and leaving behind a world worth inheriting?”

We deserve to know the answers to these — and a dozen other — questions. Why nobody in the press or Congress is asking any of them is a different story for another day.

While it’s possible that central bankers are competent, benevolent experts doing their best, it’s equally possible they are the largest economic and social vandals in all of history.

Given that possibility, the Overton Window really needs to be smashed wider, and quickly, so that we can get answers to those ‘impolite’ but necessary questions above. If it turns out that the central bankers have thoughtful, intelligent responses to them, then fine. We can debate the assumptions and data.

If, on the other hand, they get snippy and affronted by being challenged, then it will mean they have no good answers. It will unveil that they’re merely ‘winging it’ when literally everything is on the line.

It will mean, for the sake of ease and expediency, they’re basically dismantling a cultural heritage site as they scavenge for handy building materials. Turning architectural splendors into crude stone huts.

In other words, they’d be unmasked as economic and social vandals. Wrecking the infrastructure of financial knowledge and thousands of years of cultural arrangements simply because they are too intellectually lazy or too emotionally weak to do otherwise.

We Have To Be Our Own Rescuers

The Powers That Be, like central bankers and politicians, are just humans. They err. They have to operate with imperfect information.

Read More @ PeakProsperity.com

Loading...