Select date

Repos Boost Fed’s Assets by $181 Billion

by Wolf Richter, Wolf Street:

![]() Meanwhile, the Fed relentlessly sheds MBS, replacing them with Treasuries, including short-term Bills.

Meanwhile, the Fed relentlessly sheds MBS, replacing them with Treasuries, including short-term Bills.

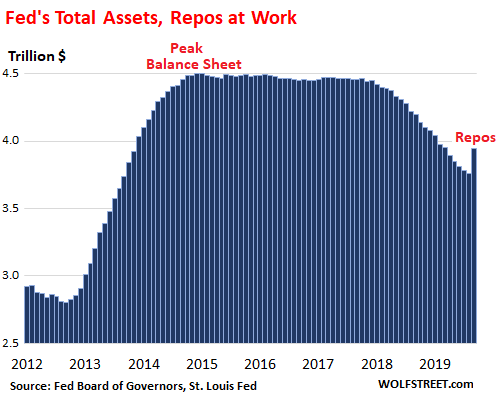

Total assets on the Fed’s balance sheet jumped by $184 billion over the past month through October 2, to $3.95 trillion, according to the Fed’s balance sheet released Thursday afternoon. This increase was mainly a result of the New York Fed’s repo operations – particularly the three repo operations with 14-day maturities that will all unwind next week:

The New York Fed used to conduct repo operations routinely as its standard way of controlling short-term interest rates. When short-term rates spiked following the 9-11 attacks, the Fed responded with a burst of repos for six days, at which point short-term rates settled down, and those repos unwound. When Lehman and AIG collapsed in September 2008, the Fed switched from repo operations to emergency bailout loans, zero-interest-rate policy, QE, and other “tools.” Repos were no longer needed to control short-term rates and were halted. Then last month, as repo rates spiked, the New York Fed dusted off its trusty old repo tool.

The New York Fed currently engages in two types of repo operations: Overnight repurchase agreements that unwind the next business day; and 14-day repurchase agreements that unwind after 14 days.

The overnight repos on the Fed’s balance sheet for the week ending October 2 amounted to $42 billion. The Fed acquired those repos in the morning of October 2, and unwound on October 3. All prior overnight repos had already unwound before the date of the balance sheet and are gone.

Overnight repos are continuing. For example, this morning (Oct. 4), the Fed accepted $38.55 billion, meaning the Fed gave market participants $38.55 billion in cash, in return for securities: It bought $29.5 billion in Treasury securities and $9.05 billion in Mortgage Backed Securities backed by Government Sponsored Enterprises. The repurchase agreements specify that the sellers (such as banks) have to buy them back the next business day (Monday), which is when those repos will unwind. Overnight repurchase agreements, though they’re not legally loans, function like overnight loans.

The three 14-day repos amount to a total of $139 billion. All three will mature and unwind next week:

- 24: $30 billion, matures on Oct. 8

- Sep 26: $60 billion, matures Oct. 10

- Sep 27: $49 billion, matures Oct. 11

So, on the Fed’s balance sheet for the week ending October 2, there were four batches of repos: one batch of overnight repos totaling $42 billion that unwound on Oct. 3; and the three 14-day repos totaling $139 billion that will unwind next week. This is how the Fed’s balance sheet on October 2 ended up with $181 billion in repos.

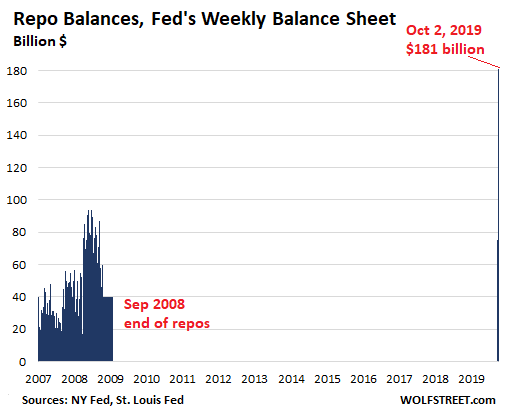

This chart shows the balances of all repos maturing within 15 days – overnight and 14-day repos combined – on the Fed’s weekly balance sheets since 2007:

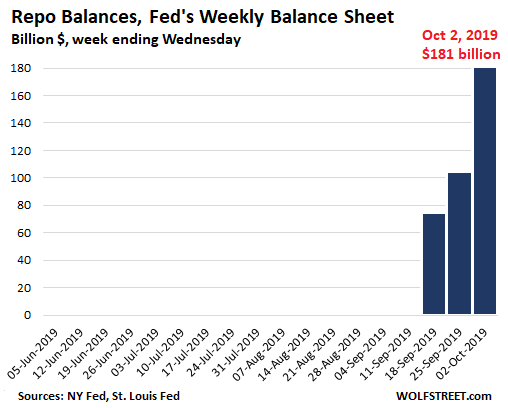

On the Fed’s balance sheet, these repo balances are carried in a separate account, called “repurchase agreements.” For more detail, this chart shows the same balances of repos maturing within 15 days but only for the Fed’s weekly balance sheets since June 2019:

Meanwhile, the MBS run-off continues and exceeds “cap” for fifth month in a row

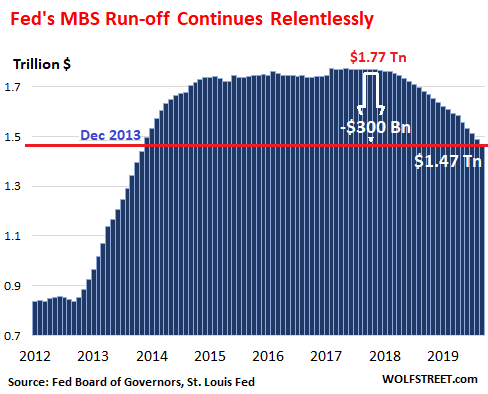

In September, the balance of Mortgage Backed Securities (MBS) from its QE program fell by $22 billion – exceeding the self-imposed cap of $20 billion per month for the fifth month in a row – to $1.47 trillion, below where it had first been in December 2013. Over the last five months, the Fed has shed $116 billion in MBS:

The Fed, like all holders of MBS, receives pass-through principal payments as the underlying mortgages are paid down through regular mortgage payments or are paid off when the home is sold or the mortgage is refinanced. About 95% of the MBS that the Fed holds mature in 10 years or more, and the runoff is nearly entirely due to pass-through principal payments.

Mortgage interest rates have fallen since November, which has triggered a surge in mortgage refinancings, and the pass-through principal payments to holders of MBS have surged as well.

The Fed has stated that it wants to get rid of the MBS on its balance sheet entirely because they’re cumbersome for conducting monetary policy. And it has stated that by holding MBS, it’s giving preferential treatment to housing debt over other forms of private-sector debt, and it wants to end assigning these types of preferences.

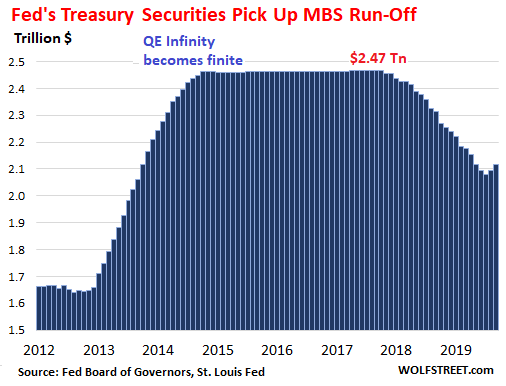

Treasury Securities pick up slack from the MBS run-off

The Fed’s stated plan is to replace all maturing Treasury securities and the MBS run-off with new Treasury securities of maturities that represent the overall Treasury market maturity mix, including short-term Treasury bills.

During September, the balance of Treasury securities rose by $22 billion, in line with the Fed’s plan to replace with Treasuries the MBS that rolled off its balance sheet over the same period. This increased the balance of Treasury securities to $2.12 trillion, including $6 billion in short-term Treasury bills. This was the second monthly increase since the end of 2017:

The thing to watch next week will be how the unwind of the three 14-day repo batches is going. Market participants have to cough up $139 billion and hand them to the Fed. This is a lot of moolah for one week and could put some strain on the repo market. So this morning, the Fed announced that has scheduled new 14-day repos and one 6-day repo, occurring three a week, through the end of October, which would make unwinding the current batch of 14-day repos a lot easier. It also said that it will continue the overnight repos through November 4.

Loading...

Humanitarian Endeavours")