Select date

Gold It’s All About Real Interest Rates Not the US Dollar

by Michael Pento, Market Oracle:

The Federal Reserve’s recent need to supply $100’s of billions in new credit for the overnight repo market underscores the condition of dollar scarcity in the global financial system. This dearth of dollars and its concomitant strength has left most market watchers baffled.

The Federal Reserve’s recent need to supply $100’s of billions in new credit for the overnight repo market underscores the condition of dollar scarcity in the global financial system. This dearth of dollars and its concomitant strength has left most market watchers baffled.

Since 2008, the Fed has printed $3.8 trillion (with a “T”) of new dollars in an effort to weaken the currency and boost asset prices–one would then think the world should now be awash in dollar liquidity. Yet, surprisingly, there is still an insatiable demand for the greenback, leading many to wonder what is causing its strength. And importantly for precious metals investors, there is a need to understand why this dreaded dollar strength has not served to undermine the bull market for gold. of text.

The primary drivers for dollar strength are growth and interest rate differentials. The Federal Reserve was able to raise overnight lending rates to nearly 2.5% and end its QE program, before its recent retreat from a hawkish monetary policy to one that is more dovish. The Fed Funds Rate now stands at 1.75-2.0%. However, the ECB and BOJ both have negative deposit rates and are currently engaged in QE. Not only this, but the extra income investors can receive owning a US 10-year Treasury Note compared to those of Japan and Germany are 175bps and 200 bps, respectively. In addition, year over year GDP growth in the EU was just 1.4% in Q2 of 2019; and Japan’s growth registered a paltry 1.0%. Growth in the US was 2.3% y/y. While that is not earth-an shattering rate of growth, it is still better than our major trading partners.

With sub-par growth and little hope for improvement on the horizon, the ECB and BOJ have decided to continue with ZIRP and QE in a futile attempt to spur growth. Nevertheless, their economies are still stagnating.

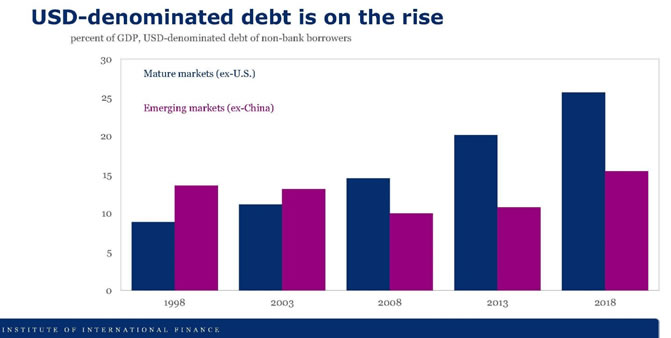

The US central bank is now being forced to lower rates once again. This is primarily due to the strengthening dollar that is hurting foreign holders of USD-denominated debt–of which there are a lot.

The BIS estimates that foreign USD-based debt now exceeds $11.5 trillion.

A rising US dollar puts further stress on these dollar-based foreign loans and makes them harder to service. In effect, this creates a squeeze on dollar shorts. When you add in the Fed’s burning of nearly $800 billion worth of base money during its Quantitative Tightening (QT) Program, you can clearly see the reasons for dollar strength.

But those who believed the US dollar would increase its buying power against gold have been dead wrong. This is because the primary driver behind the dollar price of gold is the direction of real interest rates.

Therefore, it is imperative not to measure the US dollar’s real strength by measuring it against other flawed fiat currencies that are backed by even more reckless central banks. Instead, the genuine value of the dollar should be weighed against real money…gold.

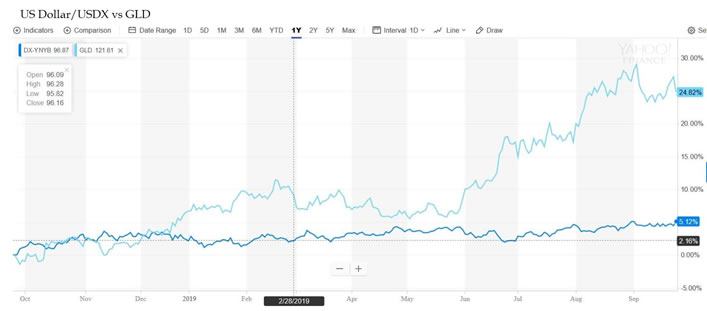

Conventional wisdom would tell you that the dollar and gold have a reciprocal relationship. When the dollar decreases in value, gold increases and vice versa. However, recently, the dollar and gold have both been strengthening in tandem. Just look at a chart of the dollar index vs the GLD.

Again, the primary driver of gold isn’t the direction of the dollar but the direction of real interest rates. Hence, if US growth is accelerating in a non-inflationary environment, gold should suffer regardless of the direction of the US dollar. Conversely, the USD dollar can be in a bull market against a basket of fiat currencies—as it has been for the past year—and yet can still lose significant ground against gold as long as nominal interest rates are falling in an environment of rising inflation.

Read More @ MarketOracle.co.uk

Loading...