Select date

The Holy-Cow Moment for Subprime Auto Loans; Serious Delinquencies Blow Out

by Wolf Richter, Wolf Street:

![]() But it’s even worse than it looks. And this time, there is no jobs crisis. This time, it’s the result of greed by subprime lenders.

But it’s even worse than it looks. And this time, there is no jobs crisis. This time, it’s the result of greed by subprime lenders.

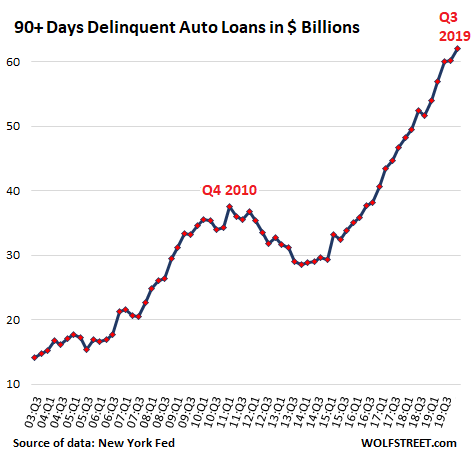

Serious auto-loan delinquencies – auto loans that are 90 days or more past due – in the third quarter of 2019, after an amazing trajectory, reached a historic high of $62 billion, according to data from the New York Fed today:

This $62 billion of seriously delinquent loan balances are what auto lenders, particularly those that specialize in subprime auto loans, such as Santander Consumer USA, Credit Acceptance Corporation, and many smaller specialized lenders are now trying to deal with. If they cannot cure the delinquency, they’re hiring specialized companies that repossess the vehicles to be sold at auction. The difference between the loan balance and the proceeds from the auction, plus the costs involved, are what a lender loses on the deal.

The repo business, however, is booming.

But delinquencies are a flow: As current delinquencies are hitting the lenders’ balance sheet and income statement, the flow continues and more loans are becoming delinquent. And lenders are still making new loans to risky customers and a portion of those loans will become delinquent too. And now the flow of delinquent loans is increasing – and this isn’t going to stop anytime soon: These loans are out there and new one are being added to them, and a portion of them will be defaulting.

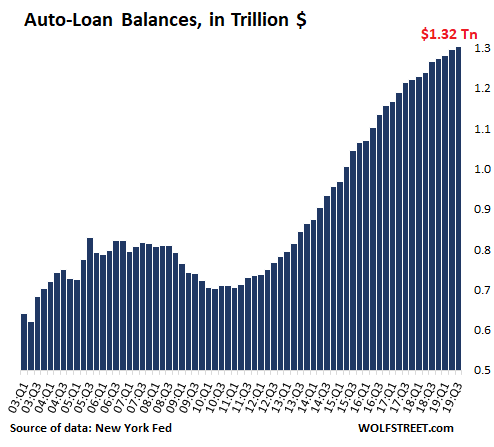

Total outstanding balances of auto loans and leases in Q3, according to the New York Fed’s measure (higher and more inclusive than the Federal Reserve Board of Governors’ consumer credit data) rose to $1.32 trillion:

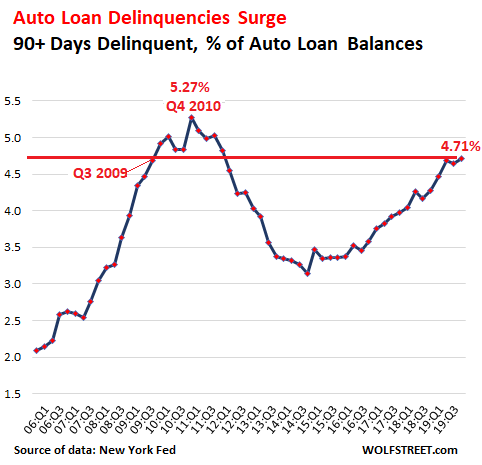

Serious delinquencies jumped to 4.71% of these $1.32 trillion in total loans and leases outstanding, the highest since Q4 2011, when the auto industry was emerging from collapse. And on the way up, this 4.71% is just above the level of Q3 2009, months after GM and Chrysler had filed for bankruptcy and a year after Lehman had filed for bankruptcy, when the US was confronting the worst unemployment crisis since the Great Depression, and when people were defaulting on their auto loans because they’d lost their jobs:

The current rate of 4.71% is just 56 basis points below the peak of Q4 2010. But these are the good times – and not an employment crisis, when millions of people who lost their jobs cannot make their loan payments.

So what is going to happen to auto loan delinquencies when employment experiences a pullback, even a fairly modest one, such as when one million people lose their jobs? That was a rhetorical question. We know what will happen: The serious delinquency rate will set a record for the annals of history.

Loading...