Select date

Lebanon Announces Default On $1.2BN Debt Payment In Historical First

Lebanon announced Saturday it will default on its Eurobond debt for the first time in its history. The protest-racked country has seen a recent change in government, banks opened for merely about half of the past few months, strict controls on hard currency withdrawals and transfers abroad amid a liquidity crisis, a plummeting Lebanese Lira since October, a run on dollars, and crushing public debt which has lately blown up to nearly 170% of its gross domestic product (now about $89.5 billion).

Prime Minister Hassan Diab confirmed in public statements the bond payment of $1.2 billion due on Monday will not be paid: “The debt has become bigger than Lebanon can bear, and bigger than the ability of the Lebanese to meet interest payments,” he said in a televised address. “We are paying the price for the mistakes of the past years. Must we bequeath them to our children?”

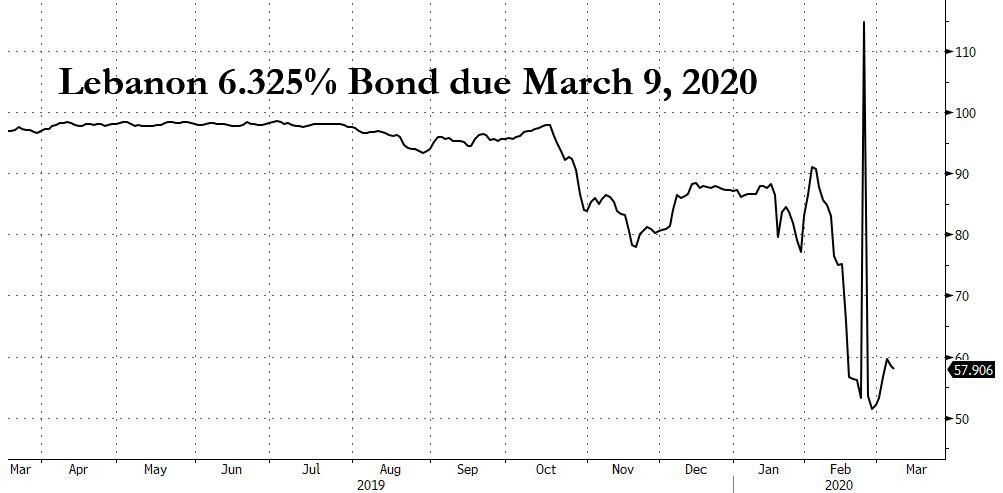

The broader crisis is being widely described as the worst and most potentially destabilizing disaster since the 1975-90 civil war. It also means that the country’s bond which mature on Monday and which last traded at a price of 57 cents on the dollar (or roughly 8000% YTM) won’t be repaid.

Local banks, which own some of the Eurobonds set to mature on March 9, have long argued against a default. But clients also fear the continued rapid depletion of their savings. Diab, appearing to respond not only to the people in the streets but to criticisms from the West centered on the Mediterranean nation’s decades of state corruption, pledged to continue negotiations to restructure the country’s debt “with all creditors… in a manner consistent with the national interest.”

“How can we pay creditors abroad when the Lebanese cannot get their money from their bank accounts?” Diab questioned, referencing controversial emergency measures banks have enacted since the start of the year, which in most places has limited account holders to withdrawing a mere $200 total a week. The Lebanese had “lived a dream that was a delusion as though things were just fine, while Lebanon was drowning in more debt,” he said further.

The domestic divide on the first ever default, which didn’t even occur during the civil war period, is further described as follows:

According to Marwan Barakat, head of research at Bank Audi, Lebanese banks owned $12.7bn of the country’s outstanding $30bn Eurobonds as of the end of January.

The central bank held $5.7bn and the remainder was owned by foreign creditors, he said.

According to local media reports, Lebanese banks have recently sold a chunk of their Eurobonds to foreign lenders.

Anti-government demonstrators who have remained on the streets since October have lobbied against repayment, fearing a depletion of reserves could further limit access to their savings.

In one of the more deeply alarming moments of his speech, Diab — who’s only been prime minister since January after the former government stepped down — cited World Bank figures forecasting that over 40% of the population could soon enter poverty. And Monday’s default, it will be even sooner.

Stretching back to last year, massive and sometimes violent intermittent anti-corruption protests have at times brought major cities to a stand-still, as the enraged public has consistently accused the national and commercial banks of “theft” while the bankers desperately attempted to defend against a massive run on the dollar and lack of confidence in the local currently.

All of this of course also comes as ill-prepared Beirut health officials deal with coronavirus, given there’s been at least 15 confirmed cases since late February.

“Whether it’s coronavirus, or any disease, or any problem, the government isn’t prepared to deal with anything,” a real estate broker told Reuters this week. It will be remarkable how often that complaint is repeated when addressing countless other governments around the globe.