Select date

Fed’s Balance Sheet Spikes as “Everything Bubble” Morphs into Financial Crisis 2

by Wolf Richter, Wolf Street:

Drags out bailout creature from Financial Crisis 1: “Loans” to Primary Dealers.

Drags out bailout creature from Financial Crisis 1: “Loans” to Primary Dealers.

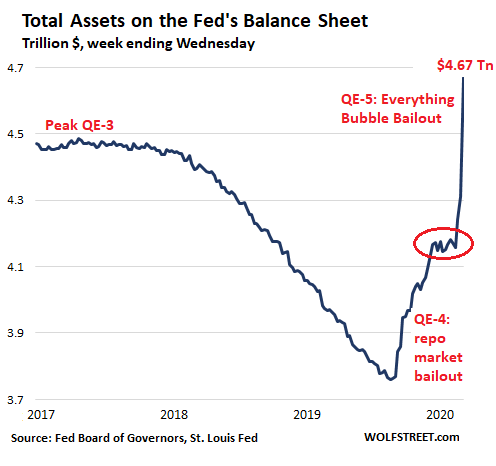

Total assets on the Fed’s weekly balance sheet, released Thursday afternoon, spiked to a record $4.67 trillion, up by $508 billion since the balance sheet of February 26, by which time all heck at already broken loose in the financial markets. Since the beginning of the repo market blowout in mid-September, total assets have ballooned by $900 billion – a result of a series of efforts to bail out first the repo market, and since the end of February, the Everything Bubble that had started imploding.

During the seven-week period between the repo market bailout (QE-4) which ended on January 1, and the Everything Bubble Bailout (QE-5) which commenced with the February 26 balance sheet, the Fed backed off QE (circled):

It’s as if the QE unwind – that drop-off in assets from early 2018 through July 2019 – had never happened. And the steepness of the new spike shows just how panicked the Fed is about the suddenly collapse of its super-bloated masterwork, the Everything Bubble that it had spent a decade inflating.

Total assets on the Fed’s balance sheet are composed mostly of overnight and term repos, Treasury securities, which include short-term Treasury bills (T-bills), mortgage-backed securities (MBS), and a newly active item, “Loans.” If the Fed gets authorization from Congress to buy old bicycles as well, they will show up as a separate line item.

The newly active bailout creature of “Loans.”

During Financial Crisis 1, the asset account “Loans” contained large balances. When the turmoil settled, those loans were paid back and the balances have since hovered close to zero through last week. But this week, this account jumped from zero to $28 billion – and this will likely soar, and we will keep our bailout eyes on it going forward.

This “Loans” account tracks the amounts the Fed has created and lent out as part of its new bailout liquidity programs. All of the $28 billion was lent to the Fed’s “Primary Dealers,” which are 24 large broker-dealers and banks that are the approved counter parties of the New York Fed. The majority are US operations of foreign financial institutions (highlighted):

- Amherst Pierpont Securities LLC (added to the list in 2019)

- Bank of Nova Scotia, New York Agency (Canada)

- BMO Capital Markets Corp. (Canada)

- BNP Paribas Securities Corp. (France)

- Barclays Capital Inc. (UK)

- BofA Securities, Inc.

- Cantor Fitzgerald & Co.

- Citigroup Global Markets Inc.

- Credit Suisse AG, New York Branch (Switzerland)

- Daiwa Capital Markets America Inc. (Japan)

- Deutsche Bank Securities Inc. (Germany)

- Goldman Sachs & Co. LLC

- HSBC Securities (USA) Inc. (UK & Hong Kong)

- Jefferies LLC

- P. Morgan Securities LLC

- Mizuho Securities USA LLC (Japan)

- Morgan Stanley & Co. LLC

- NatWest Markets Securities Inc. (UK)

- Nomura Securities International, Inc. (Japan)

- RBC Capital Markets, LLC (Canada)

- Societe Generale, New York Branch (France)

- TD Securities (USA) LLC (Canada)

- UBS Securities LLC. (Switzerland)

- Wells Fargo Securities, LLC

These Primary Dealers are the recipients of much of the bailout funds, and they also sell Treasury securities and MBS to the Fed. They’re the primary transmission channel of much of this Everything Bubble Bailout. And now, in addition to the other facilities, they’re getting direct loans under the Fed’s new liquidity programs whose proceeds they’re obligated to channel as directed by the Fed’s bailout programs.

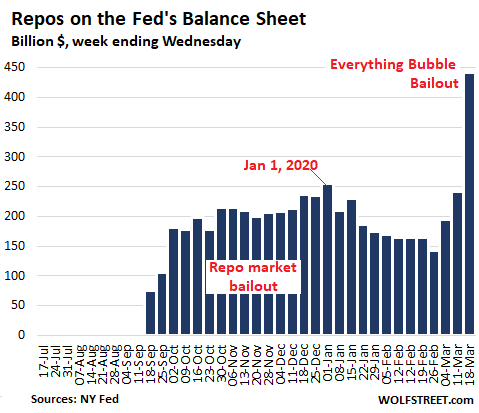

Repos spike to high heaven.

Total repurchase agreements outstanding on the Fed’s balance sheet, after plunging by 44% from January 1 through February 26, have since tripled to an all-time record of $442 billion:

The Fed is offering one-month and three-month repos of $500 billion each, twice a week, plus overnight repos of up to $500 billion, plus two-week repos, plus repo extravaganza galore or whatever.

But most of the repos are now by far undersubscribed. The Fed is essentially offering unlimited supply of cash under these repurchase agreements, far more than the counterparties can or are willing to take.

Repos are in-and-out transactions. An overnight repurchase agreement unwinds the next day: The Fed gets its money back (plus a little interest), and the counter party gets its securities back. One-month repos unwind after one month, etc.

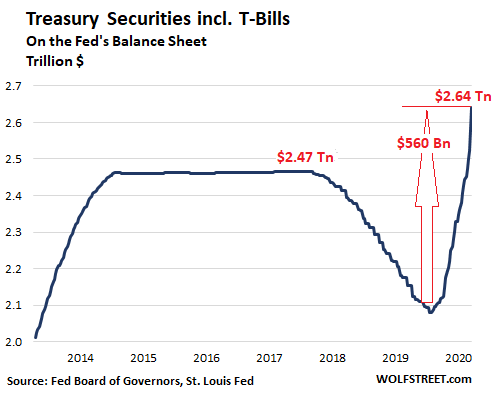

Treasury securities spike, but T-bills flatten

The Fed has restarted purchasing Treasury securities of all kinds (including TIPS and FRNs) and all maturities. But within that group, the growth of T-bill balances, which had been soaring at a rate of about $60 billion a month since the repo market blowout, has now stalled. Over the past week, the T-bill balance remained flat, with the Fed only buying enough T-bills to replace maturing T-bills.

Loading...