Select date

End of QE, Week 8: Fed’s Assets Fall by -$4 Billion for the Week, Down -$224 Billion Since June 10

by Wolf Richter, Wolf Street:

The Fed is funding consumption circuitously via Treasuries and government stimulus spending, shifting impact from asset prices to consumer prices.

The Fed is funding consumption circuitously via Treasuries and government stimulus spending, shifting impact from asset prices to consumer prices.

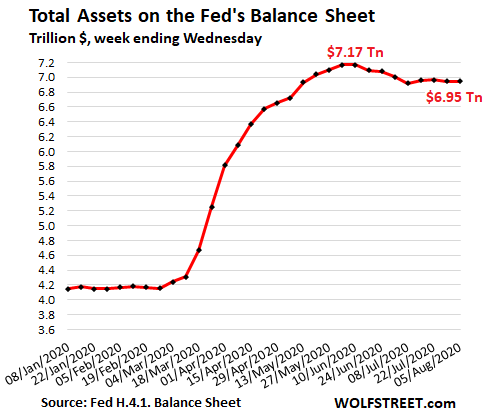

Total assets on the Fed’s balance sheet for the week ended August 5, released this afternoon, declined by $4 billion from the prior week, to $6.945 trillion. In the week ended June 10, total assets eked to a peak of $7.17 trillion. In the eight weeks then, they have fallen by $224 billion:

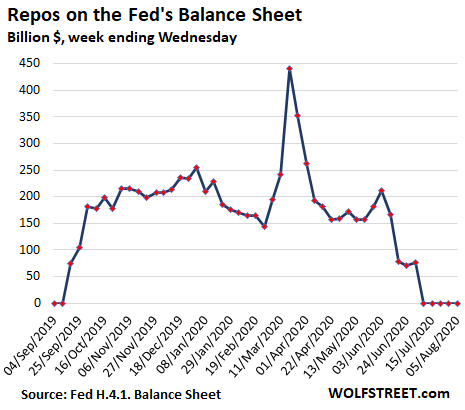

Repos continue to be zero, week 5.

The Fed is still offering huge amounts of repurchase agreements every day, but since it made them purposefully less attractive in mid-June by raising the bid rate, there have been no takers:

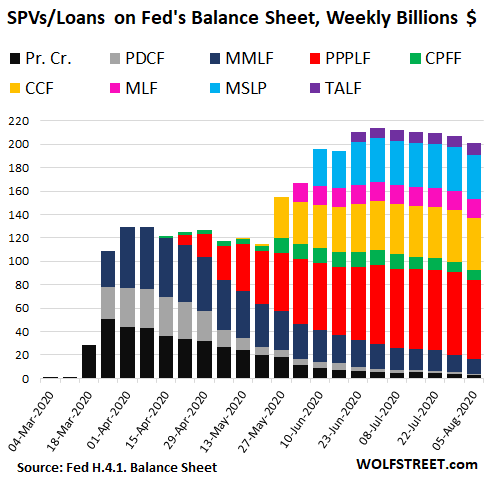

SPVs & Loans fell by $6 billion, 5th week of declines.

These Special Purpose Vehicles (SPVs) are entities that the Fed created and that it lends to. The SPV then buys assets or lends. Currently these are the active SPVs:

- PDCF: Primary Dealer Credit Facility

- MMLF: Money Market Mutual Fund Liquidity Facility

- PPPLF: Paycheck Protection Program Liquidity Facility

- CPFF: Commercial Paper Funding Facility

- CCF: Corporate Credit Facilities: includes the SMCCF (Secondary Market Corporate Credit Credit) and PMCCF (Primary Market Corporate Credit Facility). Buys corporate bonds, bond ETFs, and corporate loans.

- MSLP: Main Street Lending Program

- MLF: Municipal Liquidity Facility

- TALF: Term Asset-Backed Securities Loan Facility

In addition, there is Primary Credit (labeled “Pr. Cr.” in the chart), which are loans the Fed makes directly to banks.

Their combined balance fell by $6 billion from the prior week, the fifth week in a row of declines, to $201 billion, the lowest since June 17. The composition has changed, with the original three entities being phased out, and new ones having remained roughly stable over the past few weeks.

The largest SPV, the PPP loan facility, where the Fed buys PPP loans from banks, dropped by $3 billion to $68 billion, the first real decline since it started, indicating perhaps that some of the PPP loans are starting to be forgiven (taxpayers eat them) and are coming off the banks’ books:

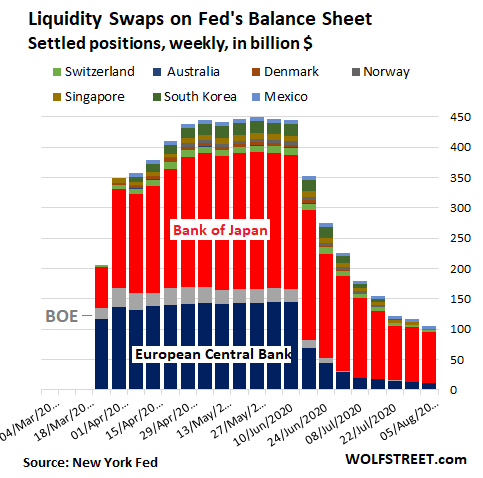

Central-bank liquidity-swaps dropped by $12 billion.

The Fed’s “dollar liquidity swap lines” were implemented and expanded during the crisis to provide dollars to select other central banks. But they have fallen out of use, as maturing swaps are rolling off without replacement. After eight weeks in a row of declines, swaps are now down to $106 billion. The Bank of Japan (red) accounts for about 80% of the total:

MBS unchanged at $1.93 trillion.

The balance of mortgage-backed securities remained at $1.93 trillion, after having dropped by $37 billion in the prior week. These balances appear erratic, for two reasons:

MBS come with pass-through principal payments as mortgages get paid off. During the current mortgage refinance boom, there has been a huge volume of principal payments that are passed through to the holders, including the Fed, reducing the balance of MBS on the Fed’s balance sheet. Just to keep the balance level, the Fed has to buy large amounts of MBS.