Select date

Subprime Auto-Loan Delinquencies, Loan Deferrals & Stimulus Curdle into Curious Phenomenon

by Wolf Richter, Wolf Street:

In the bizarre machinery of an economy that depends on consumer spending funded by stimulus and “extend and pretend.”

In the bizarre machinery of an economy that depends on consumer spending funded by stimulus and “extend and pretend.”

OK, get this: At a time when there are 29.6 million people claiming state or federal unemployment insurance because they lost their work in the worst economy of a lifetime, subprime auto-loan delinquencies, which in the past had spiked during much smaller labor market downturns, are doing the opposite: they’re dropping. Meaning, since April, people with subprime credit ratings are defaulting a lot less on their auto loans than they did during the Good Times.

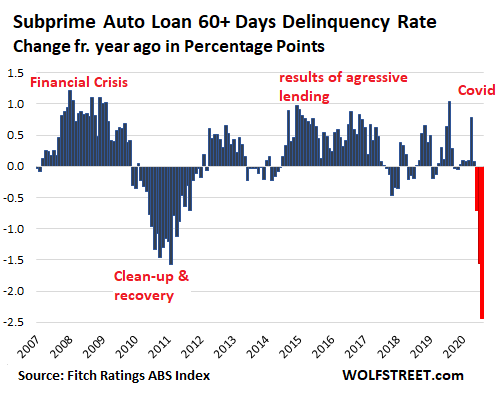

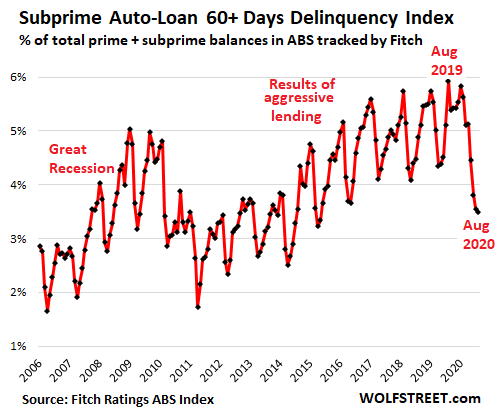

In August, delinquencies of 60 days and over of subprime auto loans that have been securitized into auto-loan Asset-Backed Securities dropped to 3.49% of total auto loans (prime and subprime), the lowest delinquency rate for any August in seven years, according to the Auto Loan Delinquency Index by Fitch Ratings. That was down 2.44 percentage points from August 2019, when the delinquency rate was 5.93%:

The 60-day-plus delinquencies started dropping in May. And given that May’s 60-day delinquencies were 30-day delinquencies in April, when tens of millions of people lost their jobs, it makes for a curious phenomenon.

This is particularly curious because from 2014 on, private-equity firms piled into the subprime auto-loan space, the lending became very aggressive, underwriting standards went to heck, and delinquencies surged as a result. But interest rates charged on those loans were so high – well into the double digits – that the game could go on, with defaults ballooning to levels far higher than during the peak of the Great Recession, and those were the Good Times.

Then we get the biggest unemployment crisis in a lifetime, and the delinquency rates should have spiked from these highs into the sky. But the opposite happened – as shown by the three red columns in the chart below, marking the change in percentage points of the delinquency rate compared to the same month in a year earlier:

So what’s going on here.

Stimulus payments and the extra $600 a week in unemployment insurance. With these funds, many strapped households had more money than they did while working. A study by the Becker Friedman Institute for Economics at the University of Chicago found that two-thirds of the people who received unemployment insurance, including the extra $600 a week, made more from UI than from working, with about 20% of them doubling their pay. And they could make their car payments, even if they had trouble making them before.

The extra $600 a week expired in July, but these are 60-day delinquencies as of the end of August – so they were 30-day delinquencies in July and transitioned into delinquency in June. And during those months, the $600 was still available. And the stimulus payments of $1,200 per adult, or $2,400 per household of two adults – and more when there are kids in the household – started going out in April and went a long way in helping make car payments over the next few months.

The $600-a-week program has now been replaced by $300 a week, and the first lump-sum catch-up checks, covering several weeks, already went out. This program is going to run out of funds in September. But for now, it’s doing its magic.

Loan deferrals – no payment, no problem. When a borrower cannot make the car payment and becomes delinquent, a lender has a choice: Either work with the customer, or repossess the car, sell it at auction, use the proceeds to cover part of the outstanding loan, and write off the rest of the loan. That can get costly.

The cheaper-for-now route is to work with the customer by putting the loan – whether it’s already delinquent or getting ready to be delinquent – into a deferral program. This kicks the can down the road.

Deferral means that borrowers are allowed to not make payments for now, but will have to make payments later, including those payments that had been missed. It’s not a free ride.

But for now, it doesn’t matter how impossible it will be for the borrower to catch up later. Because the loan is in a deferral program, the lender can mark it as “performing,” and accrue the interest income though the borrower is not making payments, and the lender can thereby “cure” a delinquency already on its books, or avoid one. The customer doesn’t have to make payments while the loan is in deferral. And everyone is happy.