Select date

“Remote Learning” Sinks Student-Housing CMBS, After Delinquencies Had Already Spiked in 2019

by Wolf Richter, Wolf Street:

The formerly hot asset class was already troubled by a multiyear decline in student enrollment and a surge in upscale supply.

The formerly hot asset class was already troubled by a multiyear decline in student enrollment and a surge in upscale supply.

“Student housing,” a subcategory of multifamily housing (apartments) in commercial real estate, is now dealing with an existential crisis – similar to retail and lodging. The mortgages backed by this once a hot asset class have been packaged into commercial mortgage-backed securities (CMBS) and sold to investors. Students aren’t exactly stable tenants. And the risks are high even in the Good Times.

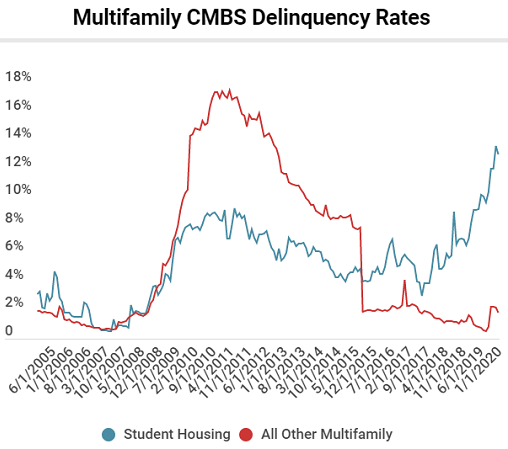

Delinquency rates of 30-plus-days on the student-housing mortgages that back $4.7 billion in “private label” CMBS (not backed by Fannie Mae or Freddie Mac) started surging in 2019, and by January 2020 hit 10%, under the impact of oversupply of student housing, particularly the trend to “luxury student housing,” that came along with the eight-year trend of declining student enrollment. And then the Pandemic washed over student housing.

The 30-plus-day delinquency rate by loan balance hit an all-time record of 13.7% in July, according to Trepp which tracks CMBS. Then in August, the delinquency rate ticked down to 13.1% (blue line), the 2nd highest ever, in part because some of the delinquencies were “cured” by entering the delinquent loans into forbearance agreements. For now, all other apartment property types (red line in the chart below) – despite the eviction bans – have shown relatively little stress, with a 30-plus-day delinquency rate at just 1.9% in August (chart via Trepp):

The straight-down plunge in the delinquency rates of all other multifamily housing types in early 2016 was in part the result of the $3-billion delinquent loan, backed by Stuyvesant/Peter Cooper Village in New York City, being resolved after Blackstone and Ivanhoe Cambridge purchased the property.

In addition, in August, the rate of student housing mortgages in “special servicing” – when a special servicer is put in charge of the loan – was 11.2%. And the rate of student housing mortgages on the servicer watchlist rose to 19.4%.

By August, $1.6 billion in mortgages backed by 101 student housing properties have requested or were already granted COVID-19 financial assistance.

Student housing is built on the foundation that students live on or near campus, and not at their parents’ place. For many people, it’s the first time living away from the parental umbrella, and it’s a blast. Or was a blast. Now colleges are struggling with the pandemic.

Some colleges are still doing remote learning only. Others have opened their campuses at reduced capacity. Some that have opened their classrooms have had new outbreaks on campus and closed their classrooms again and switched back to remote learning. For students, this is a hugely frustrating and expensive mess.

For example, one of the largest mortgages among these troubled student-housing mortgages that was granted forbearance, according to Trepp, is the $82.6-million loan, secured by The View at Montgomery, near Temple University, in Philadelphia, PA. In addition, the property secures a $9.8-million Agency mortgage that was packaged into a government-backed CMBS.