Select date

Now Everything Depends on US Stimulus, from Billionaires to China’s Manufacturers, as US National Debt Blows Out

by Wolf Richter, Wolf Street:

But consumers again paid down their credit cards; let’s be honest, that’s abuse of stimulus.

But consumers again paid down their credit cards; let’s be honest, that’s abuse of stimulus.

Who would have thought a few trillion dollars, channeled into the right pockets, could be such a big deal! Now everything depends on US stimulus: The stock market, the wealth of the wealthiest, and consumer spending – thereby not only the entire US economy but also imports from other countries, and thereby the economies of China and the rest of the world.

After yanking the rug out from under stimulus negotiations in Congress Tuesday afternoon, causing stocks to swoon, Trump today corrected his error and tried to push the rug back under the stimulus negotiations, and in addition promised voters a huge stimulus deal if they reelect him, while Biden is promising voters a huge stimulus deal if they elect him.

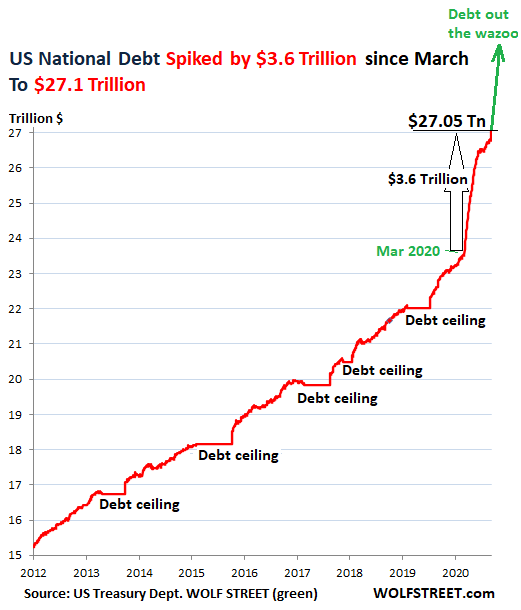

With all these trillions flying around, it’s hard to choose which trillions to go for. Meanwhile, the US national debt surpassed $27 trillion, hitting $27.05 trillion as of October 5:

Upon the news that Trump was trying to push the rug back under the stimulus talks in Congress, stocks related to retail spending soared today. Some examples:

- Amazon [AMZN] + 3.1%

- Kohl’s [KSS] + 5.9%

- Ford [F] + 3.6%

- GM + 4.0%

- Harley [HOG] + 3.0

- Delta [DAL] + 3.5%

- American Airlines [AAL] + 4.3%

- Carnival [CCL] + 5.3%

- TJX [TJX] + 3.1%

- Abercrombie [ANF] + 6.2%

- GAP [GPS] + 6.2%,

This bonanza today followed another billionaires-came-out-on-top report by UBS and PwC, cited by Reuters. The rally in stock prices since the stimulus and central-bank shenanigans kicked in globally pushed the wealth of just over 2,000 billionaires finally over the well-deserved $10 trillion mark, beating the previous record of $8.9 trillion at the end of 2019. Between April 7 and July 31, billionaires in the technology, healthcare, and industrial sectors saw their wealth (the many billions) increase by 36% to 44%. No billionaire’s billions left behind.

Meanwhile, American consumers with credit-card debt continued the awful and disappointing habit of temporarily paying down their credit card accounts – instead of passing the money on to said billionaires – with the trickle of belated stimulus checks, and belated $600-a-week and $300-a-week in extra unemployment benefits that state employment offices are finally catching up with, and whatever miscalculated federal PUA unemployment benefits for gig workers or fraudulent workers or whoever are still arriving in lump-sum payments.

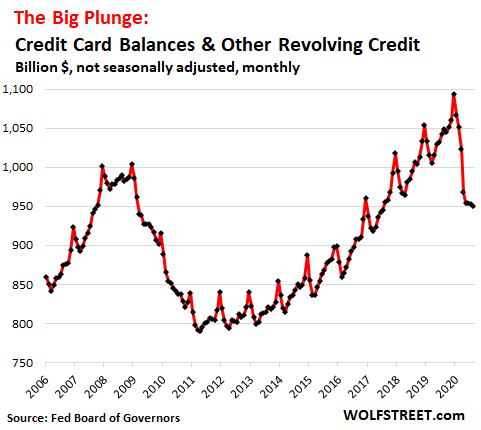

Credit card balances and other revolving credit fell “unexpectedly” by $3 billion in August, to $950 billion (not seasonally adjusted), according to the Federal Reserve today, the lowest since July 2017, and a level first obtained in September 2007:

How are banks supposed to make any money in this zero-interest-rate environment if their credit card assets that they charge 29% on are dwindling? That was a rhetorical question. Well, OK, that’s why the Fed gets frazzled when consumers pay down their credit cards. Let’s be honest, that’s abuse of stimulus.

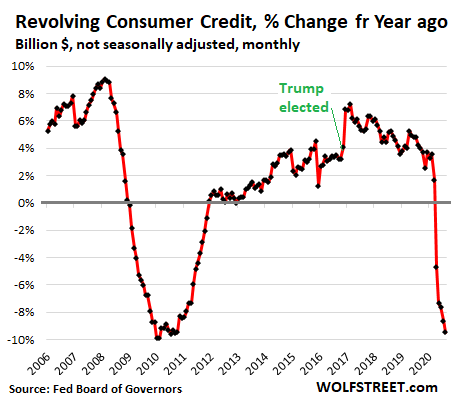

Credit card balances and other revolving credit fell a devastating 9.5% from a year ago. These declines included the record plunge in April when people used the first wave of stimulus checks to temporarily pay down their credit card accounts, so that they could charge up their credit cards later. People use credit cards as a form of cash management, like a company would use a credit line, instead of having a big pile of money in savings account. And with more room on their credit cards now, they can spend more later:

Note how during the Financial Crisis, credit card balances eventually plunged by 10%, but it took a year to accomplish that, and it was mostly done by people defaulting on their credit cards, and banks writing off the balances. Stimulus had nothing to do with it because that stimulus was only $600 per taxpayer, not $1,200, and because it came in the spring of 2008, and credit card balances continued increasing throughout 2008 and didn’t start falling until 2009.

This is not the case this time. This time, delinquent credit card balances are getting moved into a deferral program to where the borrower doesn’t have to make payments, and the lender agrees not to exercise its rights and try to collect (yeah, good luck), and therefore doesn’t need to write off the delinquent balances.