Select date

Status of the Social Security Trust Fund, Fiscal 2020: Beware of Vicious Dog

by Wolf Richter, Wolf Street:

Will Social Security Be There for You? Yes, but…

Will Social Security Be There for You? Yes, but…

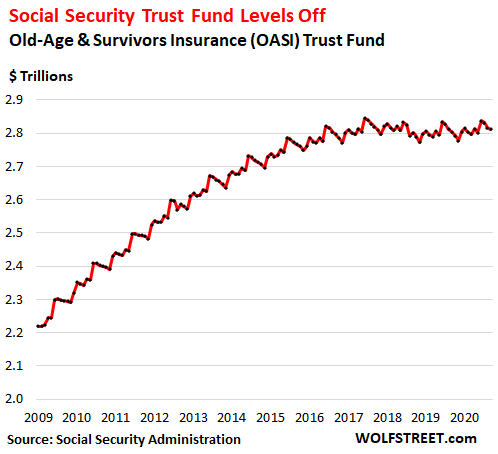

The Social Security Trust Fund – officially the Old-Age and Survivors Insurance (OASI) Trust Fund – closed the fiscal year 2020 at the end of September with a balance of $2.81 trillion, the second highest fiscal-year close, behind 2017, up by $6.8 billion from a year ago, and up by $10 billion from two years ago, according to figures released by the Social Security Administration. The Trust Fund has vacillated in the same range since 2016, after growing substantially over the past decade.

The balance is seasonal and peaks in June. The all-time peak was in June 2017, at $2.85 trillion. In June this year, the balance was $2.84 trillion. So far so good:

The Trust Fund invests exclusively in special issue Treasury securities, of two types: $2.797 trillion in interest-bearing long-term special issue Treasury securities and $14 billion in a short-term cash management security, called “certificates of indebtedness.” These securities are not publicly traded, and so their value doesn’t change from day to day with the whims of the market. The Trust Fund purchases them at face value, and the US Treasury redeems them at face value.

By contrast, a bond mutual fund that holds marketable Treasury securities must “mark to market” its Treasuries on a daily basis (producing a gain or loss).

By investing exclusively in Treasury securities that are not exposed to market whims, the Trust Fund follows the most conservative – meaning, low-risk – strategy possible.

This setup is an efficient, low-cost way of administering the Trust Fund and doesn’t allow Wall Street to extract fees and load the fund up with risks. That’s why Wall Street hates the Trust Fund and wants to “privatize” it in order to get its hands on the $2.8 trillion, extract fees out of it, and use it as dumping ground for its risks.

According to the 2020 Trustee Report, 54 million people drew Social Security retirement benefits at the end of 2019:

- 48 million retired workers and dependents of retired workers

- 6 million survivors of deceased workers.

The Disability Insurance (DI) Trust Fund is separate from the OASI Trust Fund, and is not part of this discussion here. But just to note: In 2019, it paid benefits to 10 million disabled workers and dependents of disabled workers.

During 2019, 178 million people paid into Social Security via payroll taxes. These contributions, together with interest income from the securities, generated income of $1,062 billion. Total costs of the program were $1,059 billion. A $3 billion surplus. That was for fiscal 2019.

The Trustee Report for fiscal 2020 – the 2021 Trustee Report – is not yet available, but we know already that the Trust Fund grew by $6.8 billion this year. So far so good.

Three issues: Demographics, the Fed’s interest-rate repression, and inflation.

Demographics.

For now, the Trust Fund is benefiting from millennials having entered the workforce and gaining earnings power as they move up in their jobs. But there is also the drag on the Fund of the boomers who’re now between 55 and 75 and are transitioning into retirement in ever larger numbers. For the past few years, the equation has been in balance – with millennials and boomers being both huge generations. But it will gradually change, and when it does, it will show up as a downward slope to the line in the chart above.

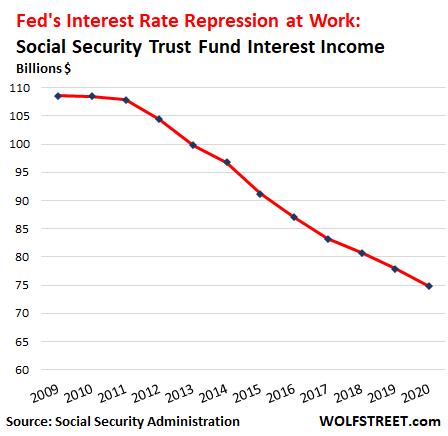

The Fed’s interest rate repression.

The effective interest rate earned by the securities in the Trust Fund has been declining for years, particularly after the Financial Crisis, when the Fed used QE to force down long-term interest rates. And the Fed’s current interest rate repression will show up as lower interest income in future years.

In September, the weighted average interest rate earned on the securities was 2.53%, still higher than current Treasury yields, thanks to long-term securities that carry the higher interest rates of yore. But since 2009, it has fallen by about half. And at current interest rate policies, the declines will continue.