Select date

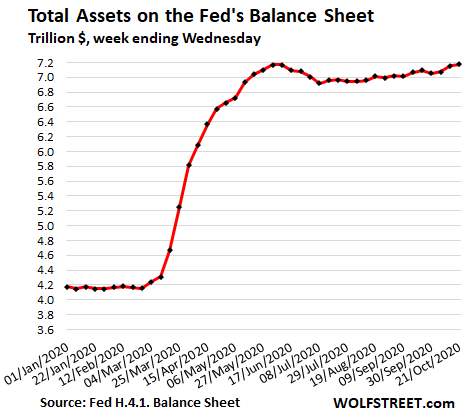

Fed Assets Eke Out New Record for First Time Since June 10. But Repos, Dollar Liquidity Swaps, SPVs Mothballed

by Wolf Richter, Wolf Street:

Only Treasury securities and mortgage-backed securities (MBS) are still active.

Only Treasury securities and mortgage-backed securities (MBS) are still active.

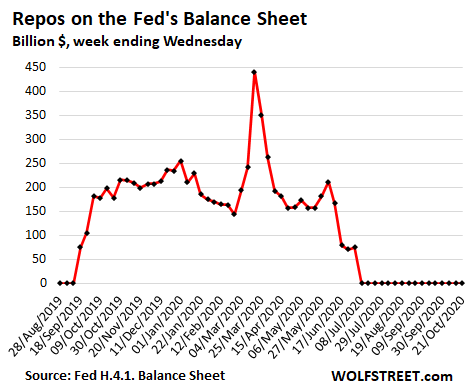

The Fed has now reduced to zero or to near-zero or essentially mothballed and thrown the towel in on three of its five QE and bailout strategies: repos, dollar liquidity swap lines, and special purpose vehicles (SPVs). It has maintained its activity in Treasury securities and mortgage backed securities (MBS).

TRUTH LIVES on at https://sgtreport.tv/

Total assets on the Fed’s balance sheet for the week ended October 21, released this afternoon, rose by $26 billion from the prior week, to $7.177 trillion, for the first time edging past the June 10 high of $7.168 trillion:

Repurchase Agreements (Repos) remained at zero:

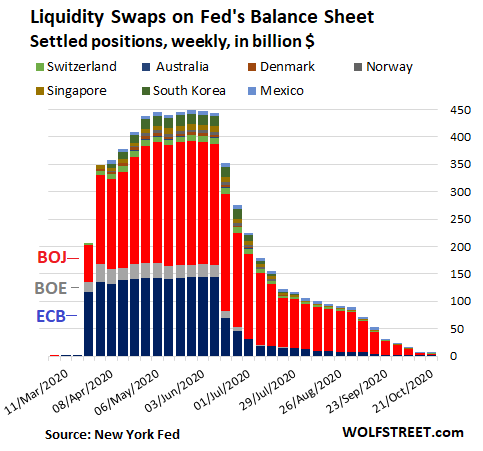

Central-bank liquidity-swaps dropped to near-zero.

The Fed’s “dollar liquidity swap lines” by which it provided dollars to a select group of other central banks, fell out of use and are down to just $7.6 billion, a mere rounding error on the Fed’s $7 trillion balance sheet, from a peak of $448 billion in early May:

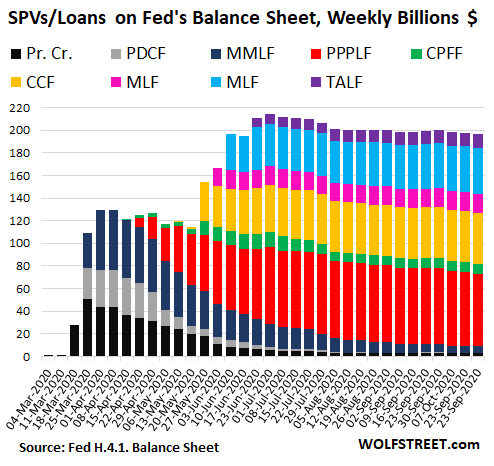

SPVs inching lower for months, now at $196 billion, mostly mothballed.

The Fed loans to the SPVs. The Treasury Department provides the equity capital. The amounts reflected in each of those SPVs is the sum of those loans from the Fed and the equity capital from the Treasury Department. But the Fed has barely lent to them, and most of the amounts you see is the equity capital from the Treasury, much of it unused, and these SPVs have now been mothballed.

Even the SPV that holds corporate bonds and bond ETFs (Corporate Credit Facilities or CCF) has been mothballed. The Fed bought its last ETF in July and only added minuscule amounts of bonds in August and September. At the end of September, the balance of ETFs and bonds was $12.9 billion, practically unchanged. The rest of the $45.4 billion in the SPV is unused equity capital from the Treasury and interest earned from the bonds. There are the SPVs:

- PDCF: Primary Dealer Credit Facility

- MMLF: Money Market Mutual Fund Liquidity Facility

- PPPLF: Paycheck Protection Program Liquidity Facility, with which the Fed buys PPP loans from banks

- CPFF: Commercial Paper Funding Facility

- CCF: Corporate Credit Facilities

- MSLP: Main Street Lending Program

- MLF: Municipal Liquidity Facility

- TALF: Term Asset-Backed Securities Loan Facility

MBS, after rising in the prior week, unchanged this week, $2.05 trillion.

The Fed and all holders of MBS receive pass-through principal payments when the underlying mortgages are paid off, such as during the current refinance boom. In addition, the MBS that the Fed buys take two to three months to settle, which is when the Fed books the trades. These two go in opposite directions, the first pushing down the Fed’s MBS balance, the second pushing up the MBS balance. And the timing is always off. Hence the erratic lin