Select date

Housing Market Goes Nuts, Everyone Sees it, But it Can’t Last

by Wolf Richter, Wolf Street:

There’s a housing shortage until there’s suddenly a housing glut: see San Francisco et al.

There’s a housing shortage until there’s suddenly a housing glut: see San Francisco et al.

Another batch of crazy housing data yesterday. Crazy in the sense that the housing market, or rather part of it, namely the higher end of it, has gone totally crazy and that by now everyone knows that this isn’t “sustainable,” that “there’s no way it can last forever,” as Redfin CEO Glenn Kelman told CNBC. And he pointed out what everyone has already been pointing out, that “part of what is fueling this boom is that the economy has just split into two, and rich people are able to access capital almost for free, so, of course, they’re going to use that money to buy homes.”

TRUTH LIVES on at https://sgtreport.tv/

But “there’s just another group of Americans who are still struggling, who can’t access the credit because we’ve raised credit standards, and you have high unemployment. I just think those two trends, at some point, have to collide.”

It’s the now well-established phenomenon of the “K-shaped recovery,” where one part is doing well, and the other part is getting crushed.

Or as WOLF STREET commenter IdahoPotato called it vastly more accurately and unforgettably, the “FU-shaped recovery.” Meaning, people who got bailed out and enriched by the Fed’s $3 trillion that it threw at the markets to inflate the prices of stocks, bonds, housing, etc. are now happy as a lark, and to heck with the rest of the people that are getting crushed.

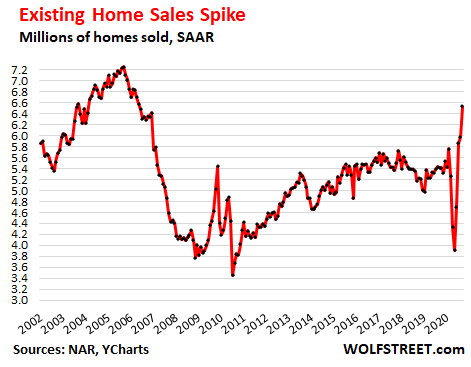

But this craziness in the housing market is not sustainable. The National Association of Realtors reported yesterday that sales of existing homes – single-family houses, condos, and co-ops – surged in September by 9.4% from August and by 20.9% from a year ago to a seasonally-adjusted annual rate of 6.54 million homes, the highest since 2006 (data via YCharts):

Seasonally, home sales normally decline in late summer and fall. But not this year. And the seasonal adjustments of the above numbers are designed for normal seasons. The NAR also releases raw(-er) sales numbers that are neither “seasonally adjusted” nor “annualized.”

On a not-seasonally adjusted basis and not annualized, 500,000 homes were sold in September, up 24.7% from September last year, the highest year-over-year increase in the data except for two months during the depth of the Housing Bust – April 2010 and November 2009 – when sales were compared to a year earlier when sales had collapsed. Sales went through some wild gyrations from 2009 through 2011.

And on this basis (not seasonally adjusted, not annualized), and compared to September 2018, homes sales were up by 34%.

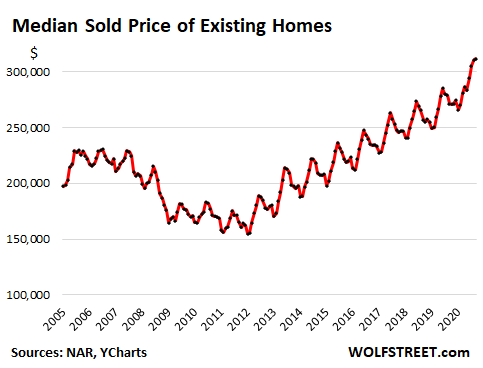

The median price of existing homes in September jumped 14.8% year-over-year to $311,800. The median price is skewed by a shift in the mix, and the price increase could also partially a result of red-hot demand for higher-priced homes (data via YCharts):

“The uncertainty about when the pandemic will end coupled with the ability to work from home appears to have boosted sales in summer resort regions, including Lake Tahoe, mid-Atlantic beaches (Rehoboth Beach, Myrtle Beach), and the Jersey shore areas,” the report said.

I have heard similar stories from real-estate brokers, such as red-hot demand in very pricy Carmel-by-the Sea, in California, about 76 miles south from San Jose and 116 miles south from San Francisco. The demand is said to be particularly hot for homes in the $2-million-plus range.

But here is what I also heard: People bought their new home without first selling their old home. They still have their place in San Francisco, or wherever, and will eventually put it on the market, but meanwhile they plowed a few million bucks into a house in Carmel and moved. These stories are everywhere.

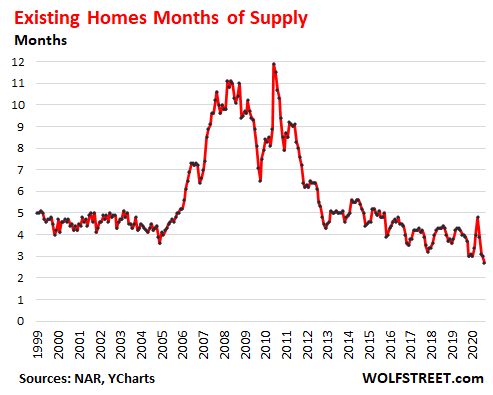

Total housing inventory of homes for sale at the end of September fell 1.9% from August and 19.2% from September, to 1.47 million homes, according to the NAR. Given the sales rate in September, this represented 2.7 months of supply, the lowest ratio in the data going back to 1999. Granted, with today’s technologies of advertising, selling, financing, and closing the sale of a home, sales take a lot less time than the did in 1999, but still (data via YCharts):

There is a shortage until suddenly there is a glut. This always surprises people.

This is happening in San Francisco — and something similar is happening in Manhattan and some other cities. The City was long described by its “housing shortage” that drove up prices and rents though there has been plenty of housing, but all high-priced, and people couldn’t afford it. And suddenly that “housing shortage” has turned into a glut. The city is flooded with a historic amount of inventory, including a record-breaking number of condos for sale, and there is a large offering of vacant apartments, and rents have plunged, with one-bedroom rents down 19% in five months.