Select date

State of the American Debt-Slaves, Q3 2020: The Stimulus & Forbearance Phenomenon

by Wolf Richter, Wolf Street:

Auto loans jump after historic price spikes. Credit cards still in stimulus wonderland. Student-loan borrowers count on debt forgiveness, mmmkay.

Auto loans jump after historic price spikes. Credit cards still in stimulus wonderland. Student-loan borrowers count on debt forgiveness, mmmkay.

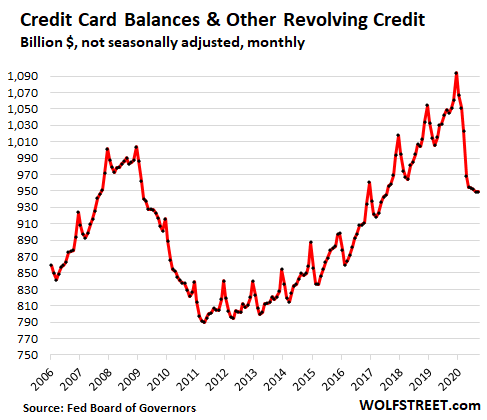

Consumers have undertaken an astounding project instead of consuming: Paying down their credit cards. In September, outstanding balances of credit cards and other revolving credit ticked down by a tad to $949 billion, not seasonally adjusted, the lowest since July 2017.

TRUTH LIVES on at https://sgtreport.tv/

Credit card balances spike in December during the shopping season and then decline during credit-hangover season in January and February. In March, they start rising again. But not this year. In March, credit-card balances fell, and then in April, when the stimulus checks arrived and when people stopped going out and spending money, credit-card balances plunged the most ever. And they have continued to tick down every month since then (not seasonally adjusted). By the end of September, according to Federal Reserve data on Friday, they were down 9.2% from September last year:

And it’s not because consumers are defaulting on their credit cards, with banks writing off the defaulted balances. On the contrary. Credit card delinquency rates have also dropped. It’s because consumers are paying down their credit cards, and they’re spending less.

They had a lot of help in form of government money – the stimulus checks and the extra unemployment benefits of $600 a week, and then of $300 a week, both now expired, and the federal Pandemic Unemployment Assistance [PUA] program for gig workers that has been surrounded by allegations of massive fraud, and so on. Whether fraudulent or not, this money got into the hands of consumers.

But many spending options disappeared: Vacations in foreign countries, cruises, even domestic flights to see friends, and the like were taken off the to-do list, and that money wasn’t spent. And some people refinanced their mortgages to take cash out of their home. And others stopped making payments on their mortgages and moved them into forbearance programs. And some people stopped paying rent, now that eviction bans are in place. And the whole flow of consumer money changed course.

This aggregate balance of revolving credit includes many people who don’t have credit card debt at all, and who pay off their balances every month. And it includes people who use their credit card as a cash management tool. They have no savings, and the money that comes in goes into paying down their credit cards that they use to pay for nearly everything. And with some of them, there is no margin for error.

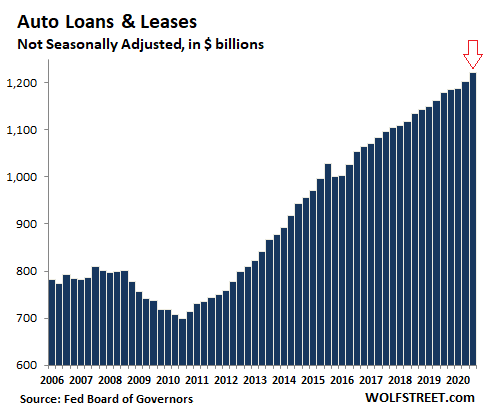

Auto loans & leases.

While consumers bought fewer new and used vehicles in the third quarter, they bought more expensive vehicles, in part because prices surged. Used vehicle retail prices spiked 15% in July, August, and September, the largest three-month spike in the data at least since 1984. New vehicle prices rose too, but people also bought more upscale vehicles – because those were the people that benefited from the Fed’s bailout of the financial markets. So they bought fewer units, but spent more dollars on them, and they took on more in loans and leases to do so.

In addition, lenders moved many borrowers who were struggling with their loan payments, or had fallen behind with their loan payments, into deferral programs to where no payments needed to be made, and the loan was not marked as delinquent, but the unpaid balances added to the overall outstanding auto loan balances.

Total outstanding balances of auto loans and leases in Q3 rose by $20 billion from Q2, to a new record of $1.22 trillion. It was the largest quarter-over-quarter increase since 2016, after having already risen by $15 billion in Q2. Compared to a year ago, balances were up by $42 billion or 3.6%:

Student loans: stalling repayments & counting on loan forgiveness.

Inexorably, student loans continue to surge, despite declining enrollment since 2010. In Q3 outstanding student loan balances jumped by $23 billion from Q2, to $1.7 trillion, and were up $54 billion from a year ago.

One of the primary factors that has been driving the loan balance up is that fewer and fewer former students made principal payments. Then came the Pandemic, and student loans were moved into automatic forbearance programs. The story I keep hearing is that you’d be a moron to make payments on your student loans because they’ll be forgiven anyway. Mmmkay. So existing loans are not getting paid down, and new loans are being added, and the balances continue to balloon: