Select date

Big City Exodus: Rents of Single-Family Houses Rise Across the US, Even as Apartment Rents in Expensive Cities Drop Sharply

by Wolf Richter, Wolf Street:

Californians applying to lease single-family houses in Arizona, Nevada & Texas doubled from year ago; migration from New York & New Jersey to Florida similar: American Homes 4 Rent.

Californians applying to lease single-family houses in Arizona, Nevada & Texas doubled from year ago; migration from New York & New Jersey to Florida similar: American Homes 4 Rent.

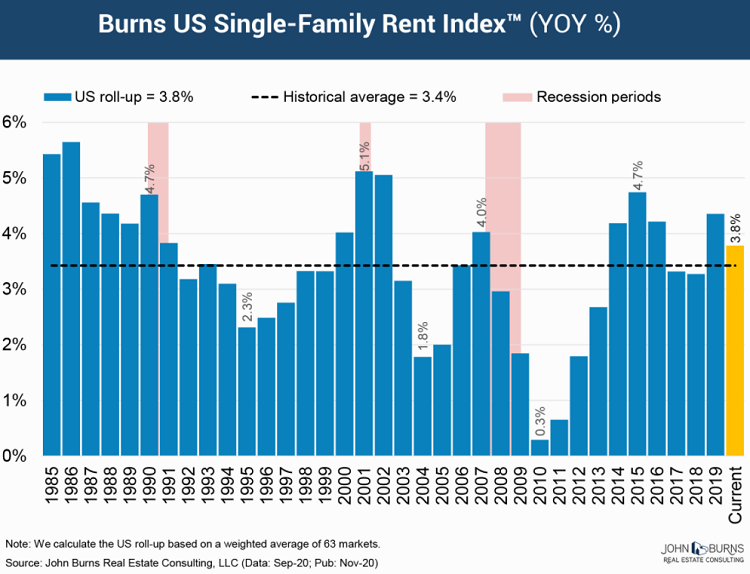

Like so many trends, the growth in the number of single-family houses for rent, and the increase in rents at those houses, preceded the Pandemic, but the Pandemic has accelerated them. In September, single-family rents across the nation rose 3.8% from a year ago, according to the Burns Single-Family Rent Index (chart by John Burns Real Estate Consulting, click to enlarge):

TRUTH LIVES on at https://sgtreport.tv/

The steepest year-over-year increases in single-family rents occurred in Kansas City (+ 7.7%), Memphis (+ 7.5%), Tucson (+ 7.4%), Phoenix (+ 7.3%) and Sacramento (+ 7.3%).

“Landlords are able to raise rents right now at a rate that is high in normal times,” Rick Palacios Jr., head of research at John Burns, told the Wall Street Journal. “It’s ridiculously high when you put it in a backdrop of a recession.”

None of the 63 markets that the index tracks showed year-over-year rent declines. The five markets with the smallest year-over-year increases were: Houston (+ 0.9%), Newark (+ 1.1%), San Jose (+ 1.2%), New York (+ 1.4%), and San Francisco (+ 1.5%).

This is in stark contrast to the apartment markets in expensive cities such as New York City, San Francisco, Boston, Seattle, Los Angeles, Washington DC, etc., where double-digit rent declines are now the rule.

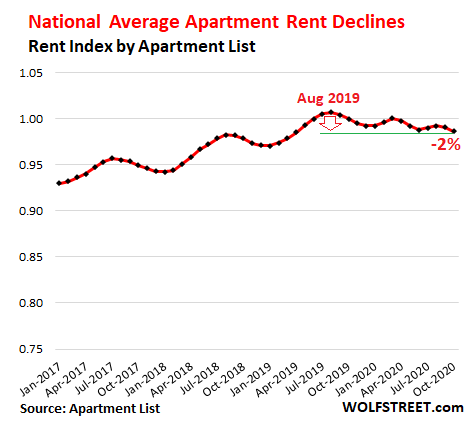

In terms of national apartment rents, the sharp declines in apartment rents in major markets has overpowered the rent increases in many smaller markets and has caused the national average rent to decline, according to Apartment List data. In October, it was down 1.4% year-over-year and 2% from August 2019:

The report by John Burns notes that the single-family rent increase of 7.3% in Sacramento occurred even though the city lost 8.6% of its jobs, which should normally put downward pressure on rents, but not this time, as rents are “likely benefiting from Bay Area transplants seeking extra space while working from home.”

This parallels the trend in the multi-family apartment market: while rents in apartment buildings plunged over 20% in San Francisco, they surged 11.5% in Sacramento.

Even within San Francisco, rents in single-family houses ticked up 1.5%, according to John Burns data, though rents in apartment buildings plunged over 20%.

Same in New York City: single-family rents ticked up 1.4% according to John Burns, while rents in apartment buildings dropped around 16%.

The five rental markets with the smallest increases in single-family rents, with the exception of Houston, are experiencing “an acceleration in outmigration fueled by COVID,” which suppressed the ability to raise rents, according to John Burns Real Estate Consulting.

Single-family rentals are big business. There are now 16.42 million single-family rental houses in the US, according to John Burns, up from 11.59 million at the end of 2006, before the Housing Bust took off.

Until the Financial Crisis, single-family rental houses were largely the playground of smaller landlords. But during the Housing Bust, PE firms, with support and encouragement from the Fed and with Wall Street funding, piled into this business, each buying tens of thousands of houses out of foreclosure, thereby becoming mega-landlords. And the number of single-family rentals surged during that time, to reach 15.6 million by the end of 2014. Since then, growth has slowed, but has continued.

These PE firms later spun off their single-family rental entities into publicly traded REITs. The largest two are Invitation Homes [INVH], with over 79,000 houses; and American Homes 4 Rent [AMH], with over 53,000 houses.

There are a number of reasons why single-family rents are holding up despite the declines in apartment rents in the largest most expensive markets, according to John Burns Real Estate Consulting:

- “Consumers placing a premium on their living space during COVID, causing an increasing amount of apartment renters to shift to single-family rentals

- “Accelerating population shift to affordable, less dense markets with diverse economies (namely Sunbelt markets where single-family rental operators are concentrated)

- “Homeowner forbearance relief preventing distressed supply from hitting the market as potential single-family rental units, which is what happened during the last recession

- “Unprecedented government assistance for consumers (i.e., extra $2,400 unemployment per month cushioning renters through July, stimulus checks, student loan payment deferrals, and temporary eviction moratoriums)

- “Extremely tight for-sale housing supply at entry-level price points, which is where single-family renters who want to buy a home typically search.”

The mega-landlords are more aggressive with their rent increases than small landlords. American Homes 4 Rent said that its new lease rates for October were up 7% year-over-year across its portfolio. Invitation Homes said that its new lease rates were up 5.5% in the third quarter, but renewals were up less, 3.3%.