Select date

Why I Think the Stock Market Cannot Crash in 2018

by Wolf Richter, Wolf Street:

![]() But the crash-insurance policy is a one-time deal. And then what?

But the crash-insurance policy is a one-time deal. And then what?

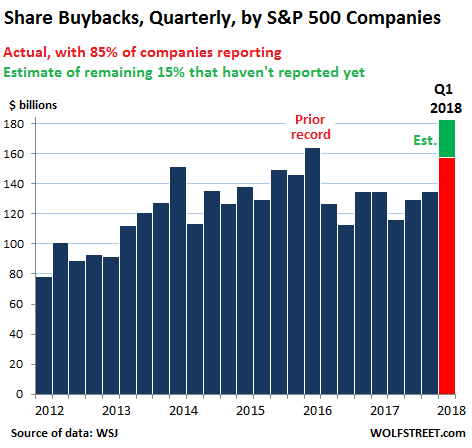

The 85% of S&P 500 companies that have reported earnings so far disclosed they’d bought back $158 billion of their own shares in Q1, according to the Wall Street Journal. The quarterly record of $164 billion was set in Q1 2016. If the current rate applies to all S&P 500 companies, they repurchased over $180 billion of their own shares in Q1, thus setting a new record:

At this trend, including a couple of slower quarters, S&P 500 companies are likely to buy back between $650 billion and $700 billion of their owns shares in 2018. This would handily beat the prior annual record of $572 billion in 2007.

Here are the top buyback spenders in Q1:

Apple: $22.8 billion

Amgen: $10.7 billion

Bank of America: $4.9 billion

JPMorgan Chase: $4.7 billion

Oracle: $4 billion

Microsoft: $3.8 billion

Phillips 66: $3.5 billion

Wells Fargo: $3.34 billion

Boeing: $3 billion

Citigroup: $2.9 billion

Buybacks pump up share prices in several ways. One is the pandemic hype and media razzmatazz around the announcements which cause investors and algos to pile into those shares and create buying pressure. Since May 1, when Apple announced mega-buybacks of $100 billion in the future, its shares have surged 11%. The magic words.

Other companies with big share buyback programs have also fared well: Microsoft shares are up 14% year-to-date. And if buybacks don’t push up shares, at least they keep them from falling: Amgen shares are flat year-to-date.

Shares of the 20 biggest buyback spenders in Q1 are up over 5% on average year-to-date, according to the Wall Street Journal, though the S&P 500 has edged up only 2%.

Share buybacks also prop up prices because they create buying pressure by the company itself when it finally does buy the shares. This is the only entity in the market that doesn’t want to buy low. It wants to buy high since it’s trying to manipulate up its own shares. By design, it provides the relentless bid in a market that might want to sell off. The amounts are huge.

In addition, share buybacks change the math of earnings per share by reducing the number of shares outstanding. The same earnings will get spread over fewer shares, thus, increasing earnings per share even if net earnings remained flat or declined. Share buybacks also counteract the dilution effects of stock-based compensation.

Share buybacks have been a godsend in this environment of rising interest rates, sky-high valuations, the QE Unwind with which the Fed is bleeding liquidity out of the market, and antsy investors.

In the first quarter, investors pulled $29.4 billion out of US stock mutual funds and exchanged-traded funds, the most since the sell-off in early 2016, according to a BofAML report, cited by the Wall Street Journal. Retail investors, after the phenomenal Trump spike, have lost their enthusiasm.

A large portion of these buybacks are now funded by corporations’ “overseas” cash. This cash accumulated in overseas entities as a result of profits that thus dodged the old US tax law. This “cash,” while registered overseas, has actually been invested in US Treasuries, US corporate bonds, and other investments in the US and elsewhere. Share repurchases were among the things companies could not do with this “overseas” cash without triggering 39% income tax. Now they can, under the reduced rates of the new tax regime.